Facts from the Week: June 11, 2022

Facts from the Week: June 11, 2022

Highlights from $COST $WSM $BBY $ASO $TGT $V $ADBE $OLLI $DKS $CAL $TSCO $BXC $RDFN $TOL $WSM $NTZ $RH $SMG $INTC

Summary

Mixed read on the consumer with Tractor Supply raising guidance and some positive commentary from Visa while some areas are soft especially home goods

Inventory levels are up but some note units are not up much while price is higher

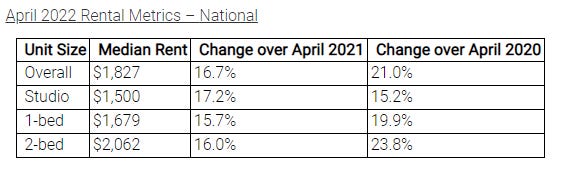

In housing, rents continue to grow 15%+ as noted by Redfin and Realtor.com

Consumer

Costco - $COST

In terms of renewal rates, we hit an all-time -- we hit all-time highs. At Q3 end, our U.S. and Canada renewal rate was 92.3%, up 0.3% from the 12 weeks earlier at Q2 end.

we're not seeing a lot of change in our throughput in the buildings. I mean we're seeing a lot of traffic. We're not seeing trade down really. We're seeing a little bit of shift in where people are spending their money. Last year, there was more stuff for the home and that -- and this year, it's more sales in tickets and restaurants and travel and tires and gas and things of that nature. But we're still hurdling our own in areas like apparel and furniture and jewelry, TVs, appliances. All those departments are showing good decent sales growth on top of pretty good numbers a year ago.

now a few comments regarding inflation. First of all, it continues. Pressures from higher commodity prices, higher wages, higher transportation costs and supply chain disruptions all still in play. For Q1, we estimate price inflation was in the 4.5% to 5% range. For Q2, we had estimated 6-ish, if you will. And for Q3 and talking to our merchants, estimated price inflation was in the 7-ish percent range. However, we did see inflation in fresh foods come in slightly lower in Q3 versus Q2 a year ago as we began cycling high meat prices. We believe our solid sales increases and relatively consistent margins show that we have continued to strike the right balance in passing on higher costs.

Finally, I want to address some incorrect information floating around on social media and a few other media outlets claiming that we have increased the price of our $1.50 hotdog and soda combinations sold in our food courts. Let me just say the price when we introduced the hot dog/soda combo in the mid-'80 was $1.50. The price today is $1.50, and we have no plans to increase the price at this time.

Visa - $V

The other thing to note is that during the pandemic, we saw a big shift to people who are essentially stuck at home buying products. You had a significant decline in consumption of services. You're seeing that pendulum swing. And so where we see the greatest growth right now is in things people couldn't do before like travel, like restaurants, like entertainment and so on. So we get the benefit of the pendulum swing, which you may not see in -- when you look at the numbers for people who sell goods.

More broadly, as we look across our income groups, we're not seeing big differences between lower-income and high-income groups. If you look at the trends relative to 2019, not only were they stable between April and May, but they've been stable for quite a few months, in fact, for several quarters now.

we're not economic forecasters. We definitely don't want to get into that business. Just based on the facts as they stand today, there's no evidence of any slowdown in consumer spending as of the 28th of May when we release those numbers.

Adobe - $ADBE

In May, consumers spent $78.8 billion online, which represents 7.1% YoY growth. It is over $1 billion more than the month prior, when consumers spent $77.8 billion online (4.5% YoY growth), and below the $83.1 billion (7% YoY growth) that was spent in March. In 2022 so far, consumers have spent a total of $377.6 billion online, growing 8.9% YoY.

“Despite the modest increase in consumer spending online, an uncertain economic climate and rising costs in core areas like groceries are putting a hamper on overall demand,” said Patrick Brown, vice president of growth marketing and insights, Adobe. “Slower consumer spending on discretionary items has driven slower, single digit e-commerce growth since March, and this pullback mirrors the easing in online inflation.”

Ollie’s - $OLLI

We were pleased with our first quarter results given that we were up against headwinds including strong stimulus-induced sales a year ago, cooler weather which impacted sales of our seasonal products, and a consumer faced with significantly higher inflation, particularly on gas and food. Our current sales trends have improved meaningfully in the second quarter fueled by increased demand for warm weather seasonal products, combined with our incredible deals and strong inventory position. We are doubling down on our efforts to offer great value as consumers continue to feel inflationary pressures, although we have not yet seen the full benefit of consumers trading down.”

Best Buy - $BBY

From a category standpoint, the biggest contributor to the comp sales decline were computing and home theater. Although down from last year's strong sales compared to Q1 of fiscal '20, our computing revenue has grown more than 30%. Our Domestic Appliance business, which has grown every quarter except for 1 for more than 10 years, delivered comparable sales growth of 3% on top of 67% growth last year.

“Macro conditions worsened since we provided our guidance in early March which resulted in our sales being slightly lower than our expectations. Those trends have continued into Q2 and, as a result, we are revising our sales and profitability expectations for the year.” -CEO

Dick’s - $DKS

However, I want to be very clear that we are not seeing any meaningful trends that are different from what we saw in Q1 and we believe our inventory at plus 40% actually is very healthy and we are very pleased with it. In fact, there are areas where if we could have more, we would have more. There's been some disruption in terms of when inventory is flowing in. But we had anticipated that certain categories, like fitness and outdoor equipment would normalize this year. And they have normalized as we expected. We are still chasing products in certain categories and our inventory is healthy. We are not anticipating any significant markdown risk.

To answer your other question, our -- the promotional environment, we are not seeing a change in the promotional environment. We will obviously continue to monitor that and we will be surgically addressing price changes as we absorb some of the cost increases. But the marketplace has not shifted dramatically in any meaningful way. We are just being appropriately cautious as we look toward a lot of things that are outside of our control when we look at the rest of the year.

Caleres - $CAL

I would say the consumer demand fundamentals, as far as we can see, remain very strong. I think we're extraordinarily fortunate that we have a portfolio of diverse brands like we have that reach so many different consumer segments and price points, along with Famous that really reaches so many consumers and has all the national brands that they really want.

So quite honestly, Dana, we have not seen any significant change in the demand of the consumer in the last number of weeks. It's still as strong as April had been and really don't believe that that's going to change that significantly for us as we move through the second quarter and through the rest of the year. Again, all to be seen, but we feel very confident in all of the signals that we're seeing about our business.

Tractor Supply - $TSCO

While there is still a significant portion of the second quarter of fiscal 2022 ahead, Tractor Supply currently forecasts net sales growth of 8% and comparable store sales growth of 5% as compared to the second quarter of fiscal 2021. Diluted earnings per share for the second quarter of fiscal 2022 is forecasted to be $3.48 or greater.

“Tractor Supply is on track to deliver record results in the second quarter on both sales and earnings. As we moved through April and the weather has normalized, we have experienced strong sales of our seasonal products. The strength of our needs-based, demand-driven business continues as the team is effectively managing inventory levels, inflationary costs, and pressures across the global supply chain. We believe we are well positioned to have a strong second quarter,” -CEO

Inventory

$COST: Our total inventory in Q3 was up 26% year-over-year versus up 19% in Q2. A couple of high-level comments regarding inventory. A material component of the increase year-over-year is inflation rather than unit growth. We continue to expand open new locations, 20 new in the last 12 months. We are lapping some low stocks in certain departments as a result of last year's high demand. And we are purposely building inventory in our e-com business, primarily in big and bulky categories as mentioned earlier in the call.

$WSM: Merchandise inventories, which include in-transit inventory, were $1,396,000,000, increasing 28.4% over depressed levels last year. Inventory on hand increased 17.7% over last year. And our units were only up 1% year-over-year, which primarily reflects the mix shift to higher AUR furniture inventory. And on a 3-year basis, our on-hand inventory was down nearly 7% to 2019 pre-pandemic levels as compared to sales that have grown over 50% over the same time frame.

$BBY: Our ending inventory was up 9% compared to last year and essentially in line with the growth of our revenue since fiscal '20. Our teams did an amazing job actively managing inventory levels as the quarter progressed in this evolving supply and demand environment. Pockets of inventory constraints still exist, but are currently isolated to certain products and vendors.

$ASO: We are pleased with the health and composition of our inventory. Our ending inventory balance was $1.3 billion, a 22% increase compared to Q1 2021. This growth was expected given the diminished inventory level resulting from the 39% sales comp last year. When compared to the first quarter of 2019, total sales increased 36%, while inventory dollars were only up 8.8% and inventory units are down 8%. This demonstrates the effectiveness of our inventory planning and allocation initiatives as we are running higher sales on less inventory compared to 2019.

$TGT: The Company is planning several actions in the second quarter, including additional markdowns, removing excess inventory and canceling orders. The action plan also includes the addition of incremental holding capacity near U.S. ports to add flexibility and speed in the portions of the supply chain most affected by external volatility; pricing actions to address the impact of unusually high transportation and fuel costs; and working with suppliers to shorten distances and lead times in the supply chain.

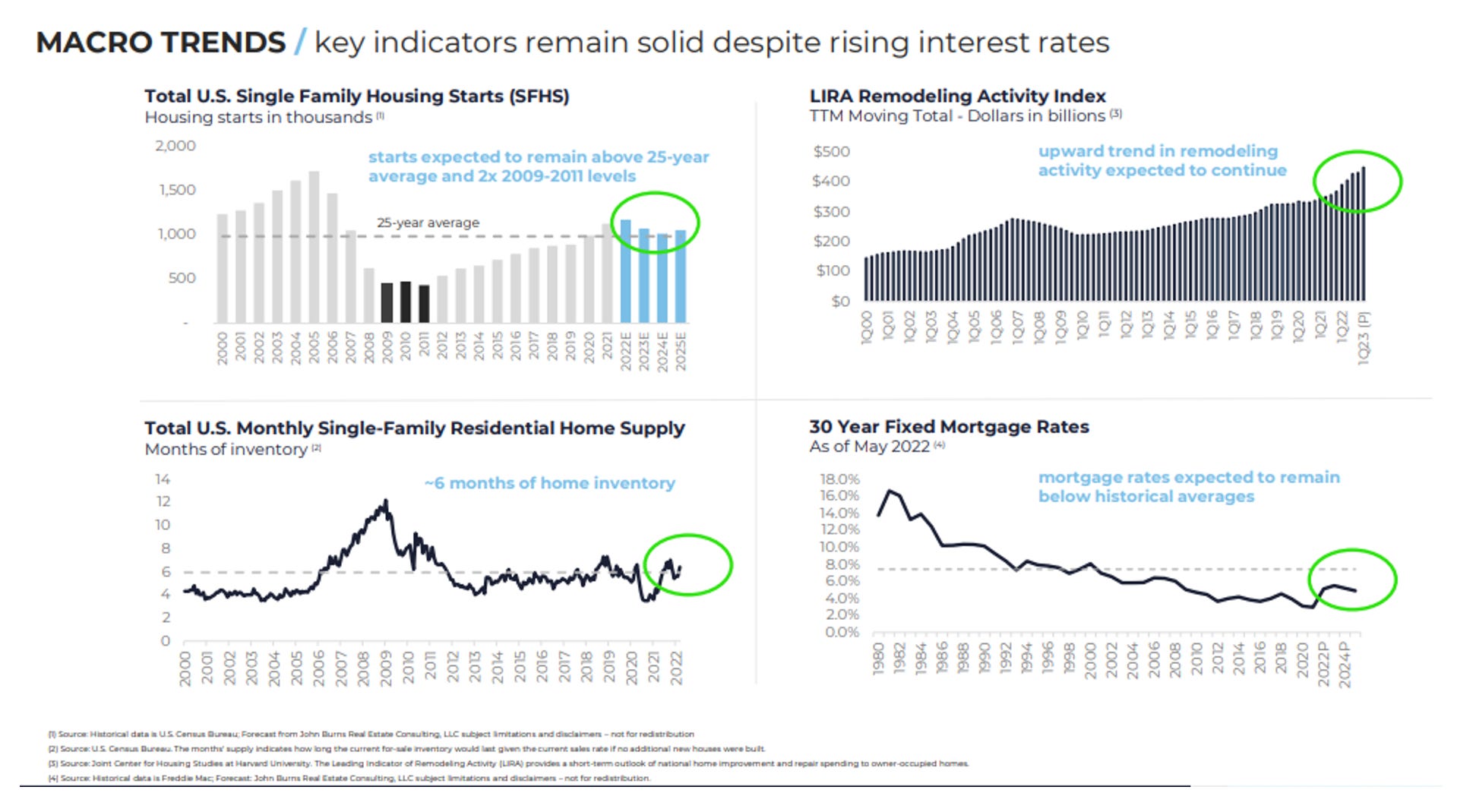

Housing

BlueLinx - $BXC

Realtor.com

Realtor.com®'s April data showed national rents maintained their record-breaking run that began in January 2021, despite posting a slightly smaller year-over-year gain than in March. The continued rent surge is attributed to the mismatch between rental supply and rising demand, largely from would-be homebuyers. Some of these aspiring homeowners are staying in the rental market for longer than they may have intended, due to intensifying cost pressures driven by both the longstanding housing supply shortage and more recent inflationary economy. If these trends continue, national asking rents will likely surpass 2022's forecasted year-over-year growth projections (+7.1%) by end of year.

Redfin - $RDFN

The median monthly asking rent in the U.S. surpassed $2,000 for the first time in May, rising 15% year over year to a record high of $2,002, according to a new report from Redfin (redfin.com), the technology-powered real estate brokerage. That’s on par with April’s annual increase of 15%, but a slowdown from March’s 17% gain.

“More people are opting to live alone, and rising mortgage-interest rates are forcing would-be homebuyers to keep renting,” said Redfin deputy chief economist Taylor Marr. “These are among the demand-side pressures keeping rents sky-high. While renting has become more expensive, it is now more attractive than buying for many Americans this year as mortgage payments have surpassed rents on many homes. Although we expect rent-price growth to continue to slow in the coming months, it will likely remain high, causing ongoing affordability issues for renters.”

Toll Brothers - $TOL

“We are very pleased with our second quarter performance, as we met or exceeded our guidance on all key metrics. We delivered 2,407 new homes and generated $2.2 billion in home building revenue – both second quarter records. Our earnings per share grew by 83% from one year ago driven by a 170-basis point improvement in adjusted gross margin to 26.1% and an 80-basis point improvement in SG&A as a percentage of revenue. In addition, we met our sales expectations with 2,874 net contracts signed in the quarter – even as we limited sales in approximately 50% of our communities. Net signed contract value, at $3.1 billion, was our highest quarter ever, driving our second quarter-end backlog to a record $11.7 billion and 11,768 homes. Based on the strength of this backlog, we are maintaining our full year projection of 20% revenue growth, a 250-basis point increase in our adjusted gross margin to 27.5%, and a return on beginning equity of approximately 23%.

“While demand is still solid, over the past month it has moderated from the unprecedented pace of the past two years as buyers adapt to higher mortgage rates and other macro-economic conditions. However, the many fundamental drivers of housing demand remain firmly in place. These include favorable demographics, the significant imbalance between the supply and demand for homes, and migration trends. We believe these factors will support a healthy housing market over the long term.

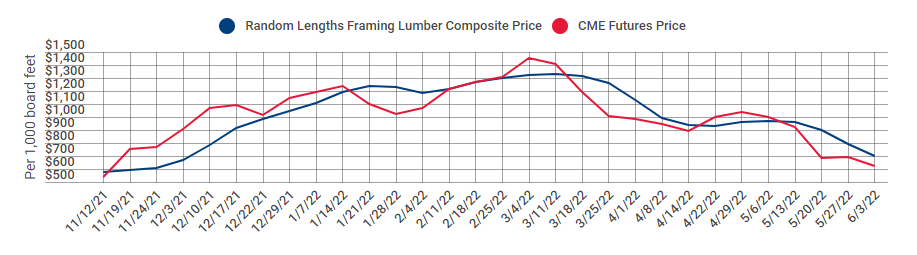

Lumber

William Sonoma - $WSM

The current economic environment is challenging, but the housing market remains strong. Hybrid work means people will continue to spend more time in their homes, and the rising costs related to gas and travel have historically led people to stay at home to cook and entertain. We believe that these 3 trends will result in continued momentum to outfit and improve the home. And as a company, we are prepared to manage through economic uncertainty. We are a multichannel portfolio of brands with a management team that has expertise and experience in managing through historical times of economic challenge.

As far as the -- I mean, first of all, the first quarter, we certainly haven't seen it. You could see it in our results with a 9.5% comp on top of the 40% last year with a 50% 2-year stack, and we said that demand is in line with that. When we're talking about the second quarter, I mean, we're really only 3 weeks into the quarter. It's super early. But we have seen some short-term moderation in demand sales within our portfolio of brands, but nothing to the degree that we're hearing others reporting out there at all.

Natuzzi - $NTZ

Since the month of April, we are seeing a more prudent approach of consumers, mainly because of the current global uncertainty. The written orders of the first 19 weeks of the year ended +19.9% above last year same period, but the more prudent attitude of the consumer is recently determining a lower traffic in our retail and in the stores of our wholesale partners.

Restrictions have been gradually lifting since the start of May. More specifically, at the beginning of May, officials of the Shanghai region allowed a limited number of our workers, initially about 20% of the workforce, and more recently up to 30%, to return to work in the factory. On 27th May, the Chinese authorities reviewed the Covid-19 restrictions again: by June 1st, our Shanghai factory will be able to have up to 85% of its total workforce in the factory. Provided that regulations will not worsen again, this will help us to significantly restore production levels starting from June. However, we expect our second quarter results to be impacted because of the limitations affecting our factory in Shanghai.

$RH

Despite our record financial performance in the first quarter, we have experienced softening demand trends which began at the time of the Russian invasion of Ukraine and have further slowed during the market disruption over the past several months.

Scotts Miracle Gro - $SMG

“Also, while it is encouraging that consumers have demonstrated lawn and garden activity remains an important part of their lifestyle, we did not see the replenishment orders we expected from our retailer partners since mid-May. In fact, retailer orders were more than $300 million below our plans for the month in the U.S. Consumer segment alone. This surprising trend has put significantly greater pressure on our fixed cost structure that, when coupled with the commodity cost increases we have experienced since the start of the war in Ukraine, will cause us to fall well short of the revised financial targets we established in March.”

Odds and Ends

Intel - $INTC

I think on the macro side, clearly, it's weaker. And we, like everyone else, will be impacted by the macro events that are unfolding here more recently. That's clearly going to impact us, as it will virtually everybody else in not only the semiconductor industry but globally in terms of corporations. For us, the other thing was we had 3 kind of headwinds coming into the quarter, which we talked about. One was the match set issue where customers could not get enough components to build product. That was we expected to impact demand. The second was inventory. We expected customers to reduce their inventory levels, which would impact their demand on us. And then there was the China, Shanghai closure and we expected that to open up in early May. And it takes time to get back to normal but get back to normal on a relatively quick fashion. I think in all 3 cases, the circumstances at this point are much worse than what we had anticipated coming into the quarter. So that certainly is an impact to the business as well. -CEO

US Federal Reserve Balance Sheet

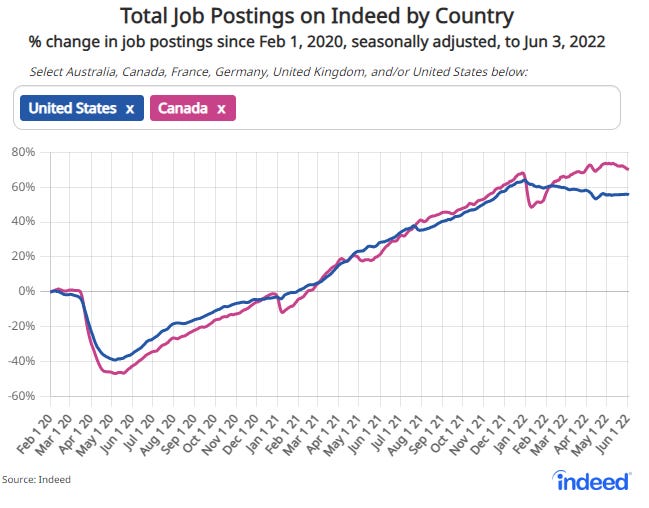

Indeed

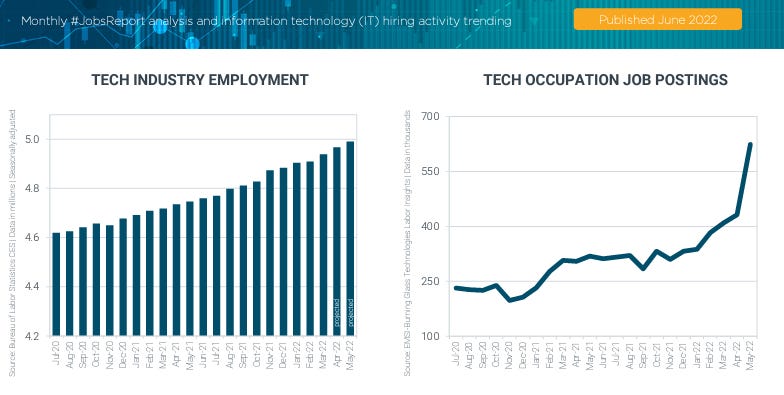

CompTIA - tech jobs

Energy Information Administration/GasBuddy

CRUDE OIL INVENTORIES:

Crude oil inventories increased by 2.0 million barrels (MMbbl) to a total of 416.8 MMbbl. At 416.8 MMbbl, inventories are 57.3 MMbbl below last year (-12.1%) and are about 15% below the five-year average for this time of year. Inventories in Cushing, OK, the NYMEX delivery point, fell 1.6 million barrels to a total of 23.4 million barrels. The Strategic Petroleum Reserve (SPR) decreased 7.3 million barrels from the prior week to 519.3 million barrels and stands 17.1% below the year ago level.

Domestic crude oil production was unchanged 11.9 million barrels per day, 900,000 bpd higher than the year ago period. While Alaska oil production fell 5,000bpd to 445,000bpd, production in the Lower 48 was unchanged at 11.5 million barrels per day.

GASOLINE INVENTORIES:

Gasoline inventories decreased by 0.8 million barrels (MMbbl) to a total of 218.2 MMbbl. At 218.2 MMbbl, inventories are down 22.8 MMbbl, or 9.5% lower than a year ago and are 10% below the five-year average for this time of year.

Freightos Baltic Index (FBX): Global Container Freight Index

Thanks for the feedback - I appreciate it and am glad you find it useful!

Those snippets of commentary from VISA and the other retailers were such valuable information for a commodity guy like me. That helps show that inflation could very well continue to grow or atleast stall rather than notably downturn. Thanks. Keep posting. I love your repots. Surprised you don't get a bit more comments subscriber grow. Keep it up and it will happen.