Secondly, we are taking a more cautious approach relative to consumer behavior in our 2022 planning given emerging pressures on consumer confidence. These include broad-based inflationary pressures and growing geopolitical risks. Looking at current trends, we have seen a deceleration in sell-through at retail over the last several weeks coinciding with these growing pressures on the consumer and are assuming a continuation of these trends in our 2022 revenue guidance.

While we typically do not give quarterly projections, we are providing first quarter guidance as we are 11 weeks into the quarter. We're expecting first quarter revenues to be between $208 million and $212 million, implying a decline of between 10% and 12%, with grill revenues expected to decline in the low to mid-20% range, offset by materially higher accessories revenue driven by MEATER.

Citi Trends - $CTRN

As we lap an extraordinary first quarter of fiscal 2021 when the March government stimulus contributed to a total sales increase of 39% vs. Q1 2019, we are planning first quarter 2022 total sales to be down 25-30% vs. the same period last year. Once we exit the first quarter, we expect our sales to accelerate as the year progresses.

Ollie’s Bargain Market - $OLLI

For the first quarter, we expect total sales of approximately $417 million to $422 million. We expect comp store sales to be down 15% to down 14% as compared to '21. On a 3-year geometric stack basis, we expect to be slightly negative in Q1 as we lap unprecedented stimulus.

will have pressures in the first half of '22, we expect improvement in our margins and metrics in the back half with the expectation of returning to our long-term algorithm.

Conn’s - $CONN

At January 31, 2022, the carrying value of customer accounts receivable 60+ days past due declined 23.1% year-over-year, and the carrying value of re-aged accounts declined 40.7% year-over-year;

Going into this year, we expected Q1 to be our most difficult quarter for the year. We are facing two major headwinds. First, the government stimulus overlap from last year and tightening by our LTO partners. We expect the impact of the government stimulus to lessen in Q2, and we will have easier LTO overlap starting in Q3.

To date, Q1 is down for comp, and you can see the impacts of the headwinds that I mentioned when you look at the monthly results. February, for example, was a positive 8% comp, while March, to date, is down 13% comp, and we expect the comparisons for April to be the most difficult in the quarter.

Rent-a-Center - $RCII

The year-over-year decline in adjusted EBITDA and margin was primarily attributable to the large swing in delinquency and loss rates between the 2 periods; predominantly in the Acima business.

As noted earlier, we believe this change in customer payment behavior is the result of the more challenging economic setting our customers experienced during the second half of 2021, which worsened throughout the fourth quarter.

Housing

Bassett - $BSET

Orders for our domestic upholstery and our outdoor products grew compared to 2021 and remain strong. Wood orders declined slightly, particularly with our imported wood products that have been susceptible to COVID-related factory shutdowns in Vietnam. Our inability to keep pace with the incessant inflationary pressures that we are experiencing cost us between 150 to 200 basis points in our consolidated operating margins for the quarter. The material cost in our upholstery operations was the biggest culprit as practically every raw material involved with manufacturing a sofa, chair or sectional has continued to escalate in price over the past eighteen months. Recognizing this, we are reluctantly implementing our sixth wholesale price increase in the new inflationary world of the last 15 months.

Corporate retail profits, on the other hand, tripled to $3.4 million in the period as higher gross margins and leverage from delivering our order backlog combined to produce better results. We also enjoyed a strong Presidents Day promotion to end the quarter, thus providing for the likelihood of continued strong retail deliveries for the foreseeable future.

TempurPedic - $TPX

“We expect that the first quarter of 2022 will be the 10th out of the last 11 quarters that we have delivered double-digit sales growth. However, while we expect double digit sales in the first quarter, recent geopolitical events, falling consumer confidence and new COVID variant outbreaks in our international markets have resulted in sales below our expectations following a strong Presidents’ Day sales period.”

Thompson continued, “We remain committed to making investments in marketing, product launches, and our operations this year to support the long-term growth trajectory of the business. However, in response to the current geopolitical uncertainty permeating the European market, we have elected to postpone the launch of the new international line of Tempur products that was planned for 2022 to the first quarter of 2023.” -CEO

Home24

Outlook 2022:

With uncertainties due to inflation, supply chains and consumer climate, home24 currently plans a currency-adjusted revenue growth between +2 % and +17 % and an adjusted EBITDA margin between +1 % and +5 %.

Acquisition of Butlers and the development of a curated marketplace as main cornerstones to strengthen the market position and create a better offering for customers, regardless of market fluctuations.

Based on the weakened market demand in the first quarter and the uncertain factors in the macroeconomy, the forecast is broadly defined and will be further specified in the course of the year. From today's perspective, home24 is planning for currency-adjusted revenue growth rates of +2 % to +17 % and an adjusted EBITDA margin of +1 % to +5 % for the financial year 2022.

Arhaus - $ARHS

“2022 is off to a strong start and we feel well positioned to deliver on our financial and operational goals in 2022. Supply chain constraints are beginning to ease on both the inbound and outbound side and we believe lead times will continue to improve. While raw material and transportation costs continue to be above historical averages, they are in-line with our expectations, positioning us to deliver on our goals for the year.”

LoveSac - $LOVE

For our fiscal first quarter of 2023, we expect net sales growth of approximately 39% and breakeven adjusted EBITDA compared to positive adjusted EBITDA of $5.3 million in the same quarter last year. Adjusted EBITDA is primarily being impacted by expected low gross margin of approximately 700 basis points year-over-year related to higher inbound ocean freight rates and higher outbound transportation costs resulting from higher fuel surcharges.

MillerKnoll - $MLKN

We expect sales in the fourth quarter of fiscal year 2022 to range between $1,075 million and $1,115 million. The mid-point of this range implies a revenue increase of 76% compared to the same quarter last fiscal year on a reported basis and 23% on an organic basis, excluding the impact of the Knoll acquisition, dealer divestiture, and foreign currency translation.

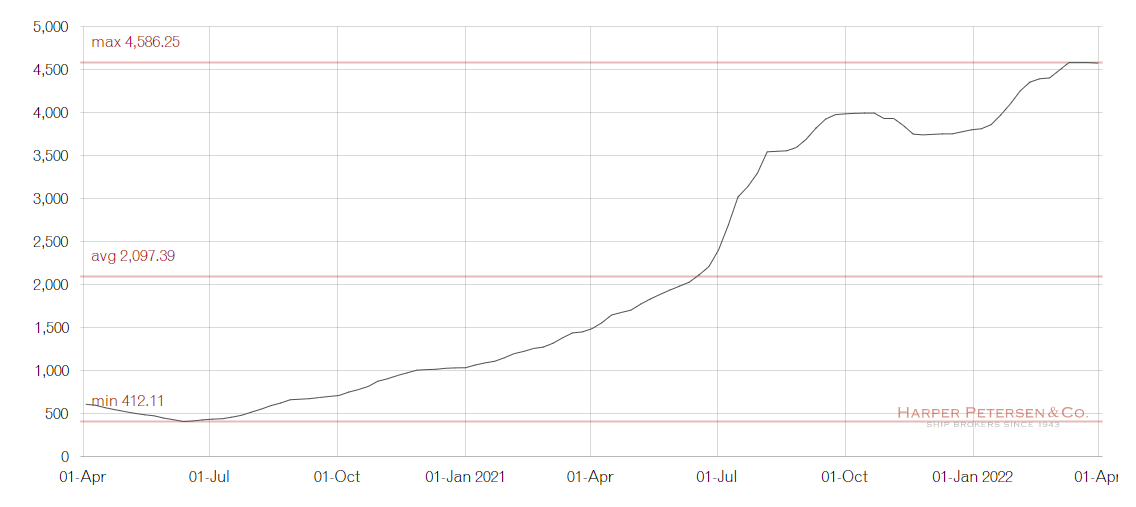

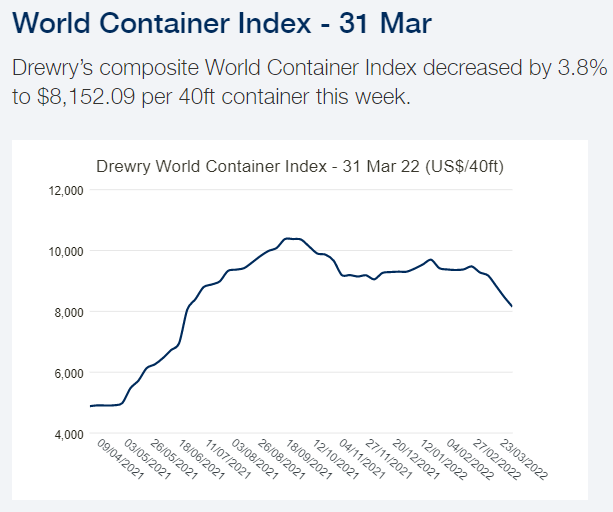

Supply Chain

Nike - $NKE

Well, maybe I'll start by just saying that Vietnam at this point in time is operational and our production volume on plan. And while transit times remain elevated, particularly getting into the North America marketplace, beginning in the fourth quarter, we're going to start seeing an improved flow of supply. And so we are increasingly confident in that reality and continue to manage that dynamic with our partners, our factory partners and our transit partners around the world.

Consumer demand continues to be incredibly strong. And while we've not been able to meet demand over the past couple of quarters, we're in a healthy pull market with that strong demand. And as a result of that, we really believe that, that sets a strong foundation for growth in the first half of fiscal '23 but for fiscal '23 in total.