Facts from the Week - March 20, 2022

Highlights from Consumer and Housing - $MA $RRGB $TLYS $ZUMZ $GCO $FOSL $SCVL $RDFN $WSM $KIRK

Consumer

US Census - Retail Sales Data

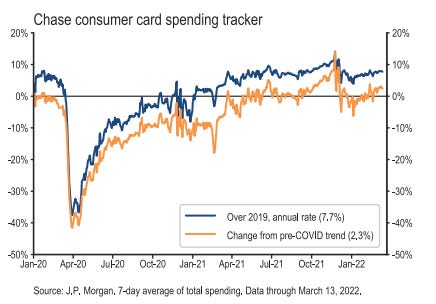

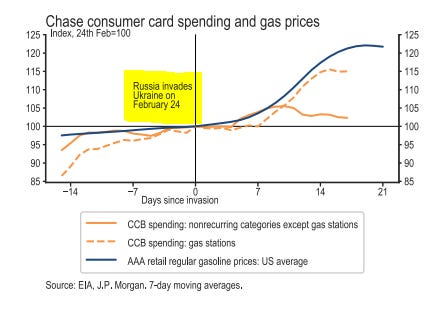

JP Morgan - Chase Spending Data

Mastercard - $MA

Opentable - Seated Diners

Red Robin - $RRGB

We currently expect to increase pricing in the mid-single digits during 2022, along with other operating initiatives underway, to mitigate cost inflation. We expect margin pressures to persist during 2022, but we expect our trajectory to improve through the year with increased staffing and dine-in sales, and reduced transitory costs. We expect to achieve 2019 restaurant-level operating profit margin in 2023.

Tilly’s - $TLYS

Through March 6, 2022, the Company's fiscal 2022 first quarter total comparable net sales, including both physical stores and e-commerce, increased by 10.4% compared to the comparable period of 2021 with an increase in net sales from physical stores of 14.0% and a decrease from e-commerce net sales of (1.3)%. Comparable net sales for fiscal February 2022 increased by a double-digit percentage, but have been negative through March 6.

During March 2021, our net sales accelerated significantly primarily as a result of considerable pent-up demand coming out of 2020's pandemic-related restrictions and significant federal stimulus payments injected into the economy, both of which were historic anomalies. As a result, the Company anticipates a further deceleration in its comparable net sales results as the first quarter of fiscal 2022 progresses compared to fiscal 2021, particularly as the Company begins to anniversary last year's peak performance in the latter half of the first quarter which was driven by the unique environment at that time.

Zumiez - $ZUMZ

Total first quarter-to-date sales for the 35 days ended March 5, 2022 decreased 1.9%, compared with the same 35 day time period in the prior year ended March 6, 2021.

Outlook: Given the positive impact of stimulus on net sales in the first quarter of fiscal 2021 and the current economic uncertainty, the Company anticipates that net sales for the first quarter of fiscal 2022 will be between $215 million and $221 million, down meaningfully to the prior year. With this reduction in sales the Company expects deleverage in the income statement related to both fixed costs as well as the re-introduction of expenses forgone in 2021 as a result of the COVID-19 pandemic such as store wages, training and travel.

Genesco - $GCO

With respect to fiscal '23, sales have gotten off to a much stronger start versus last year, but a slower start versus pre-pandemic, driven largely by the lower inventory level and lagging tax refunds. We are expecting year-over-year trends to moderate as we anniversary stimulus and the lack of inventory further pressures growth early in the new year, especially in the first quarter. Looking further into fiscal '23, we're working hard to overcome the cost pressures that are prevalent today, and we don't anticipate the factors that led to such a strong full price selling environment to be sustained.

Fossil - $FOSL

on the supply chain front, we're not seeing major business impacts from the crisis in Ukraine at this time as our supply chain doesn't include routes through the impacted areas. That said, we are watching oil prices as freight operators can pass fuel surcharges along and there could be some freight expense, or pressure if the conflict continues and oil prices remain elevated.

Shoe Carnival - $SCVL

For the first 6 weeks of fiscal 2022, net sales continued to grow, driven by strength of customer traffic gains. The second half of Q1 and Q2 go up against large government stimulus funds in the prior year, which we are not anticipating being funded again this year. As such, we anticipate the first half of 2022 to generate net sales between flat and low single-digit increase. Once we lapse the major stimulus funding, we forecast mid- to high single-digit growth for the remainder of 2022.

Housing

US Census - Single Family housing starts

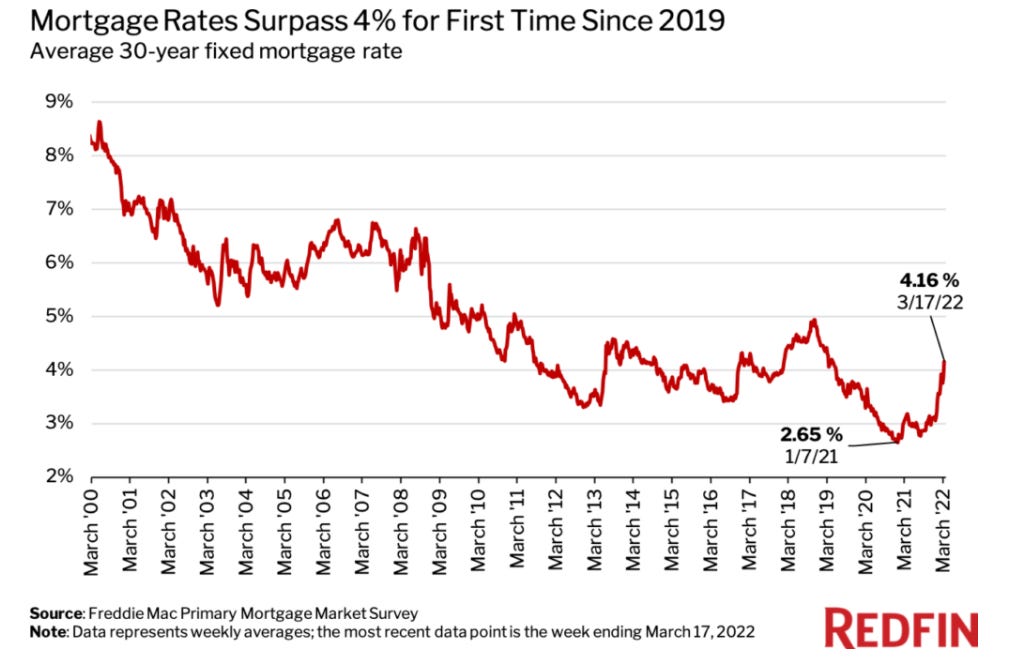

Redfin - $RDFN

The median home sale price rose 3.5% between January and February, the fastest month-over-month gain ever seen during the winter months. Prices were up 16% year over year to an all-time high of $389,500 in February as the number of homes for sale fell to another new low. The lack of inventory is holding back home sales, which fell 4% from January.

“An acute shortage of homes for sale continues to stymie buyers in the current market,” said Redfin chief economist Daryl Fairweather. “Rather than dropping out of the housing market, homebuyers only seem to be getting even more voracious, driving prices up at a startling clip. Typically, rising mortgage rates weaken demand for homes—we don’t see demand weakening yet, but we will be watching to see if buyers back off or remain steadfast amidst rising borrowing costs.”

William Sonoma - $WSM

Given the significant macro supply chain disruptions throughout the year and the ongoing strong customer demand, we are still below optimal levels. As a result, we expect to see elevated back order levels continue until the back half of 2022.

Kirkland’s - $KIRK

From a top line perspective, we expected better performance to start the quarter as we comped the negative impacts from weather last February and lower inventory levels, but the macro challenges affecting discretionary spending are currently impacting customer traffic. The margin declines are driven by higher freight costs with clearer visibility in the first half of the year [in] how much freight will exceed the prior year.

Odds and Ends

AAII Bull Bear

CNN Fear & Greed

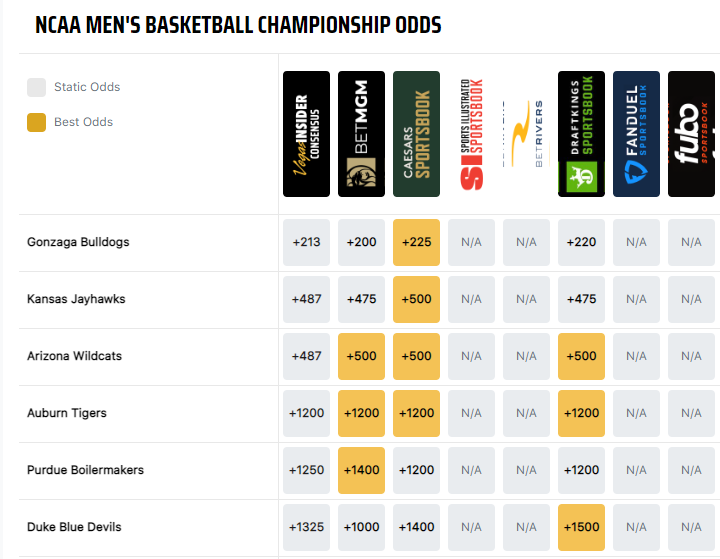

NCAA Basketball