Facts from the Week: May 22, 2022

Highlights from Recruit, $GEE $WEBR $SCVL $TGT $WMT $TJX $ROST $HD $LOW $RDFN $ZG Labor Consumer Housing

Labor

Recruit Holdings

Revenue for Q4 FY2021 increased 80.4% YoY. On a US dollar basis, revenue increased 64.7% as a prolonged period of elevated hiring activity globally led to increased demand for Indeed and Glassdoor's hiring products and services. On a US dollar basis, revenue in the US increased 57.9%, supported by demand from both small and medium sized businesses and large enterprises. Revenue outside of the US increased 86.6%, primarily led by Europe and Canada. The supply of job seekers in the labor market and active on Indeed and Glassdoor increased, but continued to be unable to fully meet the significant hiring demand from employers, resulting in continued competition for talent on Indeed and Glassdoor in Q4 FY2021.

GEE Group - $GEE

The increase in contract staffing services revenues of $2.6 million and $8.1 million, or 8% and 13%, for the three and six-months ended March 31, 2022, respectively, were primarily attributable to increased demand in our professional contract services markets as the negative effects of COVID-19 lessen and the U.S. economy and workforce continue on recovery paths toward pre-COVID-19 conditions.

Industrial staffing services revenues were $3.7 million and $7.8 million for the three and six-month periods ended March 31, 2022, respectively, compared with $4.0 million and $9.1 million for the three and six-month periods ended March 31, 2021. The decline of $0.3 million, or 7%, and $1.3 million, or 14%, for the three and six-months ended March 31, 2022, respectively, was mainly due to reoccurrence of adverse conditions associated with COVID-19 variants, which caused disruptions in the industrial markets we serve and resulting in a decrease in demand for our industrial staffing services.

Direct hire placement revenues for the three and six-months ended March 31, 2022, were $5.9 million and $12.0 million, up 61% and 71%, respectively, as compared with $3.7 million and $7.1 million, for the three and six-months ended March 31, 2021. The increase in demand for the Company’s direct hire services was due to increased employment opportunities and placement orders in our professional services markets, which also coincides with lessening of COVID-19 severity and as the U.S. economy and workforce continue to trend closer to pre-COVID-19 conditions.

Consumer

April Retail Sales - US Census

Weber Grills - $WEBR

Net sales decreased 7%, to $607 million, from $654 million in the prior-year quarter. On a two-year stack basis, net sales increased 46% above 2020. Foreign exchange accounted for $20 million of the sales reduction, and, excluding the impact of foreign exchange, net sales declined 4% year-on-year. Net sales were adversely impacted by product and component part availability resulting from global supply chain disruptions. In addition, retail traffic, both in-store and online, slowed broadly in comparison to last year, driving lower category point-of-sale performance. The decrease in sales volume was partially offset by certain pricing actions.

Shoe Carnival - $SCVL

On a 3-year basis, we captured significant share growth since 2019 or 3 years ago. The consumer did not have the discretionary funds available in Q1, and the inflation, as I said, was a challenging headwind. We're seeing that already mitigate in the early part of this quarter and are very encouraged with the early trends we're seeing in the first weeks of we're seeing the consumer now get into a more normalized state and accelerated growth compared to 2019, to your question.

Q1 was truly an anomaly with the inflationary shocks, I think, consumers were digesting. We're seeing them get into a more normal stage in these first few weeks of Q2 and very pleased with the growth being able to deliver in line with the 4% to 7% guidance.

Target - $TGT

Our first quarter gross margin rate was well below our expectations, reflecting a combination of factors that prove to be very different than expected, driven by a rapidly shifting macro backdrop and changing consumer behavior. More specifically, we saw much higher-than-expected rate and transportation costs and a more dramatic change in our sales mix than we anticipated. This resulted in excess inventory, much of it in bulky categories, which put additional strain on an already stretched supply chain.

In our other 3 core merchandise categories: apparel, home and hard lines, we saw a rapid slowdown in the year-over-year sales trend at the beginning of March, when we began to annualize the impact of last year's stimulus payments. While we anticipated a post-stimulus slowdown in these categories and we expect the consumer to continue refocusing their spending away from goods and into services, we didn't anticipate the magnitude of that shift. As I mentioned earlier, this led us to carry too much inventory, particularly in bulky categories, including kitchen appliances, TVs and outdoor furniture. And with very little slack capacity after 2 years of unprecedented growth, we faced elevated cost to store and indicate a rightsizing our inventory position. Nevertheless, we're still seeing healthy overall spending by our guests, even as their spending continues to evolve.

Also notable, in comparing this year's weekly sales of pre-pandemic levels at the beginning of 2019, we're actually seeing stronger 3-year growth trends in recent weeks compared with the beginning of the first quarter, even in categories where we saw a rapid slowdown on a 1-year basis.

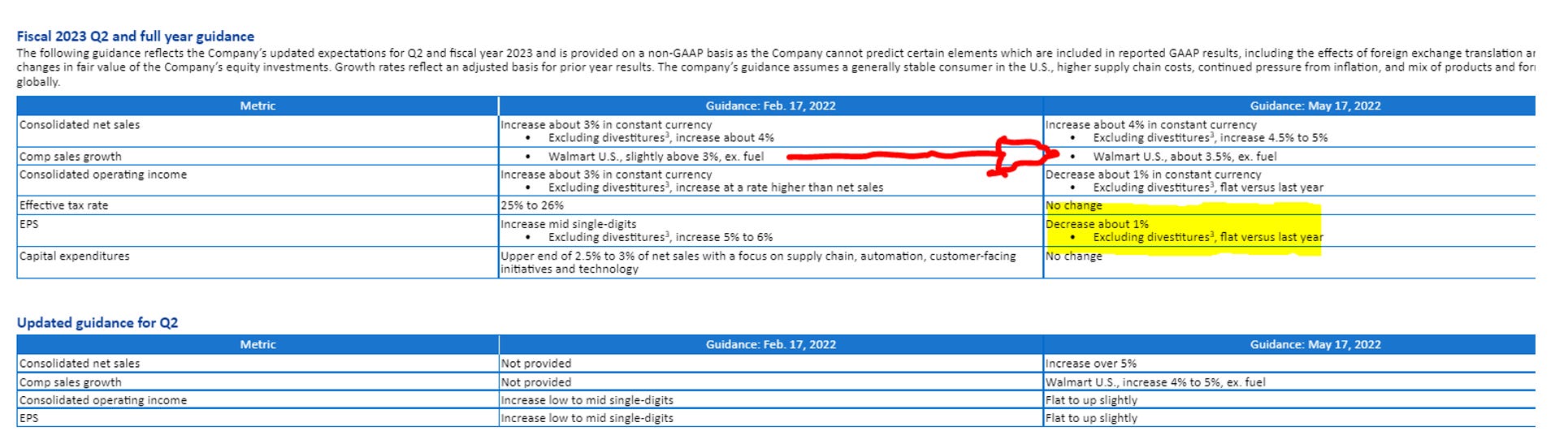

Walmart - $WMT

The first item is wage expense. As the Omicron variant case count declined rapidly in the first half of the quarter, more of our associates that were out on COVID leave came back to work faster than we expected. We hired more associates at the end of last year to cover for those on leave, so we ended up with weeks of overstaffing. That issue was resolved during the quarter, primarily through attrition.

The second item relates to our general merchandise inventory level, primarily in Walmart U.S. GM was a lower percentage of total sales in Q1, resulting in an unfavorable gross margin mix. We also had higher costs for containers and storage, and we've taken and are taking steps to contain those cost pressures to the first half of this year.

The third item is related to fuel costs in our supply chain. So those are the 3 items. And now I'll share more detail on each to help provide clarity.

TJ Maxx - $TJX

During the quarter, we saw very strong comp sales in our overall apparel business at Marmaxx, which was up 6%. U.S. home comp sales, including our HomeGoods division and Marmaxx home categories were down 7%. I should note that last year, our U.S. open-only home comp sales increased over 40%. Importantly, we believe the comp sales decline in our U.S. home businesses was a result of the difficult year-over-year comparison and not driven by our pricing initiative.

As Ernie mentioned, we are pleased to be raising our guidance for full year adjusted pretax margin to a range of 9.6% to 9.8%. This is 10 to 30 basis points higher than our original plan. I'd like to highlight that this contemplates our expectation for better flow-through on lower planned sales, which speaks to the strength of our flexible off-price model.

Our implied back half guidance is for a 4% to 5% increase over a 14% increase in the second half last year.

We're pleased with the start of the quarter with the momentum from the March, April period continuing into May to date. I should note that our second quarter comp plan reflects this acceleration in comp trends we saw in the March, April period and into May.

Ross Stores - $ROST

“We are disappointed with our lower-than-expected first quarter results. Following a stronger-than-planned start early in the period, sales underperformed over the balance of the quarter. We knew fiscal 2022 would be a difficult year to predict, especially the first half when we were facing last year’s record levels of government stimulus and significant customer pent-up demand as COVID restrictions eased. The external environment has also proven extremely challenging as the Russia-Ukraine conflict has exacerbated inflationary pressures on the consumer not seen in 40 years.”

She continued, “First quarter operating margin of 10.8% was down from 14.2% in 2021, reflecting the deleveraging effect from the same store sales decline combined with ongoing headwinds from higher freight and wage costs that began rising in the second half of 2021.”

Housing

Housing Starts - US Census

Home Depot - $HD

The Pro is very strong, and we posted those results with very much delayed spring. In Q2, it's early, but we're off to a strong start. We also think that the fundamentals -- I mean these are all very short-term in nature comments, but the fundamentals for home improvement remain incredibly supportive. So when you look at inflation and interest rates in any fatigue, if I take those in order, inflation is definitely higher than we thought. If you recall, last year, we thought we'd have about 5% growth in ticket. We're seeing obviously much higher than that with 11% in ticket. A lot of that is inflation-driven.But our customers are resilient. We are not seeing the sensitivity to that level of inflation that we would have initially expected.

So let's talk about interest rates. I think it's important to remember that our addressable market is the 130 million housing units occupied in the U.S. plus probably, call it, 40 million to 50 million more in Canada and Mexico. Of those 130 million housing units, on any given year, only about 4% or 5% are sold. That means that over 95% of our customers are staying in place. They're not shopping for a mortgage. Nearly 40% of those homes are owned outright. Of those who have mortgages, about 93% of those mortgages are fixed rate. So when you think about our addressable market, the vast majority aren't really paying attention to mortgage rates. And what we've -- what's interesting about that is what we've heard, when they do look at moving, they're actually more and more tempted to stay in their low fixed rate mortgage and remodel their home instead. So these low locked-in mortgages are probably a benefit to an improvement.

Lowe’s - $LOW

Redfin - $RDFN

Nationwide, 60.7% of home offers written by Redfin agents encountered competition on a seasonally adjusted basis in April, the lowest level since March 2021, according to a new report from Redfin (redfin.com), the technology-powered real estate brokerage. That’s down from a revised rate of 63.4% a month earlier and 67.4% a year earlier, and marks the second-consecutive monthly decline.

The housing market has softened in recent weeks because mortgage rates have surged to their highest level in more than a decade as the government tries to quell inflation. The average 30-year fixed mortgage rate is now 5.3%, up from 3.76% at the start of March and a record low of 2.65% in January 2021. The rise in rates and home prices has sent the typical monthly mortgage payment for homebuyers up a record 44% year over year to an all-time high of $2,427.

Zillow - $ZG

U.S. home values continue to grow at a record pace, up 20.9% in the past year. The combination of rising prices and a spike in mortgage rates means the monthly mortgage payment on a typical home is 52.5% higher than it would have been a year ago.

Rising costs have not yet eased competition. Homes are selling as fast as they ever have — after only seven days for the typical home — and nearly half of homes are selling for above their list price.

There are faint signs the market is starting to rebalance, including growing inventory and a rise in listings with a price cut.