Facts from the Week: May 7, 2022

Highlights from $MA $COST $SHOP $EBAY $STKS $BGFV $DHX $AMN $FRG $LGIH $LEG $SMG $ZG $BXC $RDFN $CZR $ABNB $W $RILY

Consumer

Mastercard - $MA

Costco - $COST

Shopify - $SHOP

The timing of Omicron easing was also a factor with mobility resuming with vigor earlier in Q1 of this year versus Q1 of last year, causing a shift in consumer spend to offline retail and travel starting in early February this year in strong contrast to a year ago, where that shift occurred in late March and into April. Another factor that impacted year-over-year GMV growth more than expected, although to a lesser extent than mobility, was inflation at a record level, pushing more consumer spend, both online and offline, toward discount retailers in Q1 of this year as consumers' wallets were stretched from higher prices, including a surge in gas prices due to the war in Ukraine.

Ebay - $EBAY

Let's take a closer look at our performance in Q1. Gross merchandise volume declined 17% as we lapped a 7 point sequential acceleration during 2021 and which was driven by global mobility restrictions and U.S. stimulus payments. As compared to our pre-COVID baseline in Q1 of 2019, GMV grew 7%. We were extremely pleased with the pace of growth, innovation and execution with our focused categories during Q1, coming off a record surge in growth in early 2021. Trading card volumes appear to be stabilizing at a quarterly run rate, more than double pre-COVID levels, indicating continued healthy demand in this asset class. Excluding trading cards, year-on-year growth in focused categories outpaced the remainder of our marketplace by approximately 9 points.

For the full year, we are lowering our FX-neutral growth forecast for GMV by approximately 5%. The strengthening U.S. dollar also reduces our spot GMV outlook by roughly $1.3 billion versus our prior guidance. We now expect GMV of between $73.2 billion and $75.2 billion in 2022, representing a decline between 12% and 10%. We forecast revenue of $9.6 billion to $9.9 billion, representing a decline of between 6% and 3%.

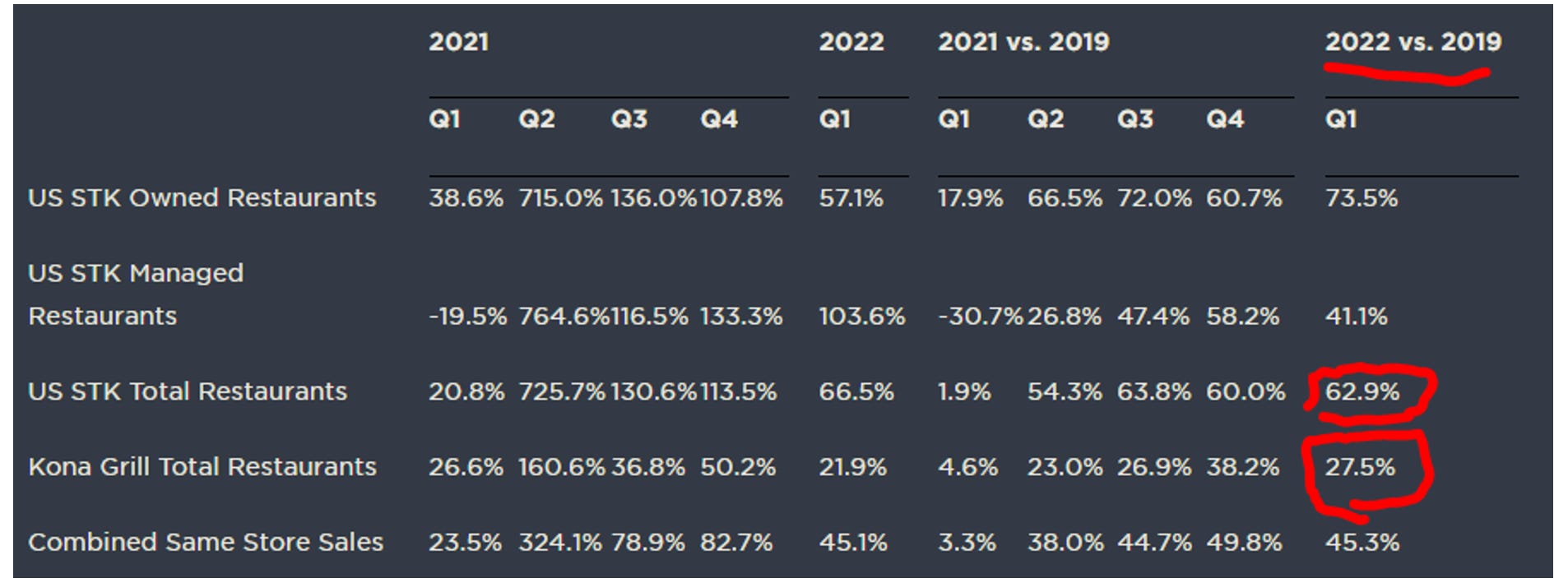

STK - $STKS

Big Five - $BGFV

For the fiscal 2022 second quarter, the Company expects same store sales to decrease in the high teens compared to the record sales of the fiscal 2021 second quarter, when net sales were more than $82 million, or 34%, higher than any pre-pandemic second quarter in the Company’s history. As a reminder, sales in the second quarter of fiscal 2021 benefited from strong pent-up demand following an easing of pandemic-related restrictions in many of the Company’s markets. The Company’s sales guidance reflects an expected same-store sales increase in the high single-digit range versus the pre-pandemic fiscal 2019 second quarter.

Vista Outdoor - $VSTO

Now let's move on to Sporting Products segment. Sales for the segment were up 56% to a record $464 million and up 55% to $1.7 billion for Q4 and fiscal '22, respectively, year-over-year. This sustained success in Sporting Products is another data point that demonstrates how the new ammo consumer is different today compared with prior surges. We have seen continued and steady demand for ammunition even as firearm indicators have slowed.

For example, as of the fiscal year-end, we had a backlog of over $3 billion. As we've said before, traditional firearms and related indicators are not necessarily correlated with ammo, which is a consumable. For example, we are seeing more sustained participation from legacy users as well as the 14 million new first-time firearms owners in the current surge in ammo demand. Channel inventories remain low for most calibers, apart from small rifle ammunition products like those produced at the Lake City Army Ammunition Plant. Purposely, we are less reliant on Lake City small rifle ammunition sales due to the Remington acquisition and our strategic shift into product mixes that are more stable and more profitable, such as hunting, personal defense and shotshell ammunition.

So for Sporting Products, we talked about that we will grow mid-single-digit for the year. But you will see Remington started ramping up last year as we were moving towards the year and the quarter. So -- and we've also guided Q1 so actually, you will see more growth in Q1 in Sporting Products.

Labor

DHI Group - $DHX

I'm happy to report that we again delivered outstanding financial results for the quarter, with total bookings growth of 32% year-over-year and total revenue growth of 29% as more employers are using our subscription-based offering.

As demand for technologists continues to grow at a rapid pace and the unemployment rate remains at an all-time low, employers need our growing community of technologists and our sophisticated tool set to find, attract, engage and hire the highest quality tech professionals. During the first quarter, U.S. employers posted 1.1 million tech jobs, 43% more than a year earlier, according to Information Technology Trade Group, CompTIA. At the same time, Dice's proprietary annual salary report, which we shared in January, indicated that average tech salaries increased 6.9% from 2020 to 2021.

AMN Healthcare Services - $AMN

Strong healthcare demand in the first quarter was met with the tightest labor market we have ever seen. Our healthcare professionals and AMN team members worked relentlessly to help address the needs of the healthcare community, reaching our highest placement volume in Company history, We achieved record performance in our nursing, allied, locum tenens, interim leadership, search, language services, VMS, MSP and RPO businesses in the quarter."

"We set expectations last quarter for staffing demand, pay rates and corresponding pricing to trend down to more sustainable levels, and we are pleased to see that the market is moving in line with our expectations, While the pressure of the pandemic has eased, healthcare organizations are still understaffed due to a severe labor shortage, high attrition, changing workforce preferences, and intense competition for professionals. These conditions are driving a greater need for our powerful portfolio of diversified solutions. The opportunities ahead for AMN are greater than ever before." -CEO

Revenue in the second quarter of 2022 is expected to be 56-61% higher than prior year. Revenue guidance includes $65-70 million from labor disruption activities. Excluding labor disruption, Nurse and Allied Solutions segment revenue is expected to grow 57-60% year over year. For the Physician and Leadership Solutions segment, revenue is expected to be approximately 20% higher than prior year. Technology and Workforce Solutions segment revenue is expected to grow by approximately 45% compared with the year-ago period.

Supply Chain

Franchise Group - $FRG

And now I think I feel better that we can see the light at the end of the tunnel because the consumer generally is challenged. And as that demand is lower, it actually solved the supply chain issues to one extent. It solves ultimately the pricing issues that we're seeing.We're seeing container costs down in some places over 50% from the peak already. And although that takes time to flow through the P&L. I think that that's a very different trend than we've seen over the last couple of years.

Freightos

Housing

LGI Homes - $LGIH

“Despite supply chain headwinds, we delivered strong first quarter operational results. Our average sales price was a record $341,495, representing an increase of 23.9% over the first quarter of last year. Absorptions for the quarter came in at 6.0 closings per community, per month, significantly outperforming our historical average of 5.5. Additionally, we delivered record profitability in virtually all our key metrics, including our highest gross margin and adjusted gross margin in Company history and new first quarter records in pre-tax net income margin and net income margin.

“As expected, cost pressures and supply chain disruptions continue to impact our operations and we are working side-by-side with our trade partners and the municipalities where we operate to limit those impacts on our customers. Additionally, while demand for new homes continues to outpace supply, it is clear we are no longer operating in the frenzied atmosphere that dominated our industry at this time last year. However, despite early signs that demand is moderating, the primary constraint to closing more homes continues to be extended cycle times and delays in the opening of new communities.

“Based on our performance to date, we are updating our full year guidance to reflect our new expectations of delivering an average sales price in a range between $335,000 and $350,000, gross margins between 27.0% and 29.0% and adjusted gross margins between 28.5% and 30.5%.” [Note: was $315-330k and 28-30% adjusted gross margin previously]

Leggett and Platt - $LEG

Sales in our Furniture, Flooring & Textile Products segment were up 17% versus first quarter of 2021, primarily from raw material-related selling price increases and volume recovery in Work Furniture, partially offset by lower volume in flooring products, textiles and home furniture.

In Home Furniture, the market demand at mid-level and upper price points remains relatively strong. However, demand at lower price points has softened. This is impacting our business in China. The Chinese market also has been impacted by COVID-related lockdowns.

Work Furniture sales have recovered to above pre-pandemic levels from strong demand for products sold for residential use and improvement in contract markets as companies redesign their footprints and invest in office space to attract and retain employees as more people return to the office. We expect continued growth in this business in 2022.

Scotts Miracle Gro - $SMG

On a fiscal year-to-date basis entering May, consumer purchases of the Company’s lawn and garden products at its largest four retailers in the U.S. are down 12 percent from the same period a year ago. The Company said the category gained significant momentum in recent weeks after a late break to spring and planned delays of promotional activity until after the Easter holiday.

“Spring weather, frankly, has been lousy in most markets and the season broke about two to three weeks later than normal,” said Jim Hagedorn, chairman and chief executive officer. “Fortunately, consumer purchases have gained considerable ground in recent weeks. For example, key early-breaking markets in the south are down mid-single digits entering May after being down double digits two weeks earlier. The combination of improved weather, strong retailer promotions through Memorial Day, and favorable comparisons for the balance of the season should be tailwinds for the rest of the year. Still, we now believe the low end of our sales guidance range for U.S. Consumer of plus-or-minus 2 percent from last year’s performance is our most likely outcome.

Zillow - $ZG

We continue to see low levels of inventory down 23% year-over-year in March. New for-sale listings were less strained in March, up 36% from February levels, but still down 9% year-over-year. Average page views per listing were at a record high in Q1, which results from low inventory, yes, but also signals a strong intent to move. These dynamics drove home values up an astonishing 21% year-over-year in March, despite rising interest rates, which of course, exacerbate affordability challenges.

So while we know people are still eager to move, market conditions are making it increasingly difficult. The net result of all of these factors is that total consumer transaction value growth trends are meaningfully softening and even the most respected prognosticators have disparate views of what will happen next.

BlueLinx - $BXC

“Net sales grew by approximately 27% year-over-year, and we delivered adjusted EBITDA of $202 million and adjusted EBITDA margin of over 15%, both all-time highs on a quarterly basis for BlueLinx.”

“We currently believe near-term fundamentals for the U.S. housing industry are healthy despite the recent rise in mortgage rates and broad-based inflation. Specifically, we believe high levels of home equity, housing turnover, and aging housing stock will continue to support growth in repair and remodel activity and the low supply of available homes will continue to drive investment in both existing and new homes.” -CEO

Redfin - $RDFN

The median home sale price was up 17% year over year—the biggest increase since August—to a record $396,125.

The median asking price of newly listed homes increased 16% year over year to $408,458, a new all-time high.

The monthly mortgage payment on the median asking price home rose to a record high of $2,404 at the current 5.27% mortgage rate. This was up 42%—an all-time high—from $1,688 a year earlier, when mortgage rates were 2.96%.

Pending home sales were down 4% year over year, the largest decrease since mid-February.

New listings of homes for sale were down 6% from a year earlier, and have been down from 2021 since mid-March.

Active listings (the number of homes listed for sale at any point during the period) fell 18% year over year.

56% of homes that went under contract had an accepted offer within the first two weeks on the market, up from 54% a year earlier, down less than a percentage point from the record high during the four-week period ending March 27.

Travel

Caesars - $CZR

And if you think about margins in Las Vegas, we were a little over 40.5% in January. In March, we were a little over 47%. The strength has continued into April. April was the single largest month in the history of the Caesars organization for cash room revenue. Occupancy was just under 97%. Rates were up a little less than 40% over last year -- last April and a little less than 20% over '19. So Vegas is extraordinarily strong for us as we sit here today. I would expect us to break the record again in May for cash hotel revenue.

AirBNB - $ABNB

Guests are booking more than ever before. In Q1 2022, gross nights booked grew 32% compared to Q1 2019 despite ongoing pandemic concerns, the war in Ukraine, and macroeconomic headwinds. People are becoming increasingly confident in booking travel further in advance, with lead times even surpassing 2019 levels by the end of Q1. Looking ahead, we see strong sustained pent-up demand. As of the end of April 2022, we had 30% more nights booked for the summer travel season than at this time in 2019, and the growth from 2019 is higher the further we look out this year.

Kayak

Wayfair - $W

With rising prices across the retail universe and amidst troubling geopolitical events, our mass customers in the U.S. and internationally appear understandably more focused on where they are spending their next dollar, pound or euro. Consumer spending is still climbing for retail overall. However, even with the relatively healthy individual balance sheet, shoppers are nonetheless diverting a larger share of their wallets to nondiscretionary categories and reprioritizing experiences like travel. Reflecting these trends within our business, we are seeing more strength from luxury and professional customers vis-a-vis mass shoppers and stronger overall performance in the U.S. relative to our international geographies.

Odds and Ends

B. Riley - $RILY + $14m of insider buying this week

https://www.insidearbitrage.com/2022/05/inside-arbitrage-friday-wrap-may-6-2022/

CNBC ran its "Markets in Turmoil" special Thursday night which apparently has a perfect track record:

Wayfair lags Overstock. Wayfair has fulfillment issues. I'm bewildered by the info on Wayfair. If anyone disagrees I will come back with facts and data.