Facts from the Week: Oct 24, 2021

Facts from the Week: Oct 24, 2021

Highlights from $ADBE $FL $TSCO $CLAR $PG $CROX $RMS $POOL $RMX $ZG $RHI $RCRT $IBKR $FCFS Consumer Housing Staffing Financials

Summary

In housing, The Joint Center for Housing Studies predicts remodel activity to accelerate in coming quarters while Pool Corp reports strong backlogs through 2022

Adobe predicts online holiday sales to increase 10% this year on top of 33% last year while international travel will open in the US November 4th helping further drive brick-and-mortar holiday sales

Consumer activity remains strong as Tractor Supply reported a 40% two-year comp

Consumer

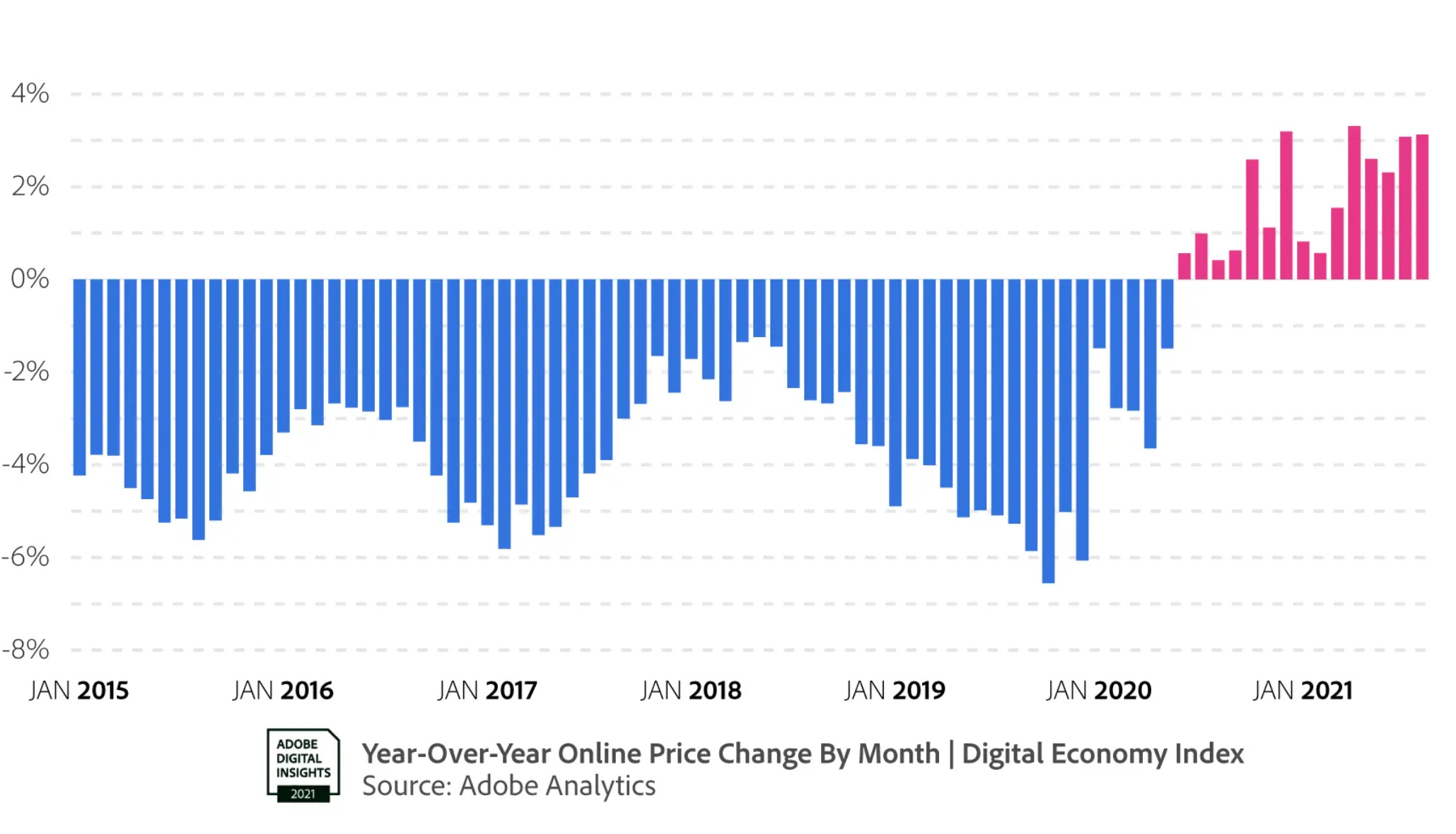

Adobe - $ADBE - online sales forecast

Adobe expects U.S. holiday sales online to hit $207 billion from Nov. 1 to Dec. 31, setting a new record. This represents a 10 percent increase from 2020, a strong growth rate after a year where the pandemic made e-commerce an essential service.

Globally, online spending is expected to hit $910 billion this season, 11 percent growth year-over-year (YoY). Adobe expects over $4 Trillion ($4.1T) to be spent globally in all of 2021 — a new milestone for e-commerce.

Foot Locker - $FL

Excellent presentation from John Zolidis of Quo Vadis Capital - he does very high quality work and knows the consumer sector as well as anyone:

https://quovadiscapital.com/

U.S. to lift restrictions Nov 8 for vaccinated foreign travelers

U.S. international air passenger traffic was down 43% in August and overall passenger air traffic was down 21% over pre-pandemic levels, the U.S. Transportation Department said Friday.

https://www.reuters.com/world/us/exclusive-us-partly-lift-international-travel-curbs-nov-8-official-2021-10-15/

Tractor Supply - $TSCO

Comparable Store Sales Increased 13.1% on Top of 26.8% Comparable Store Sales Growth Last Year

Clarus - $CLAR

By brand, the Company now expects sales for Black Diamond to increase 27% to $217.5 million ($215 million prior) and Sierra and Barnes combined to increase 99% to $105 million ($95 million prior) compared to 2020. The Company continues to expect sales for Rhino-Rack to be $40 million for the second half of 2021.

Procter and Gamble - $PG

We continue to expect organic sales growth in the range of 2% to 4%. Our solid start to the fiscal year increases our confidence in the upper half of this range. We expect pricing to be a larger contributor to sales growth in coming quarters as more of our price increases become effective in the market. As this pricing reaches store shelves, we'll be closely monitoring consumption trends. While it's still early in the pricing cycle, we haven't seen notable changes in consumer behavior.

Crocs - $CROX

Our third quarter was exceptional, underscored by 73 % revenue growth over 2020 and industry -leading operating margin of 32 % . Globally, our teams are managing through the supply chain disruptions to mitigate the impact on our business . Despite the temporary disruptions, we expect 2022 revenues to grow over 20 % from 2021 fueled by the strength of our brand and consumer demand globally -CEO

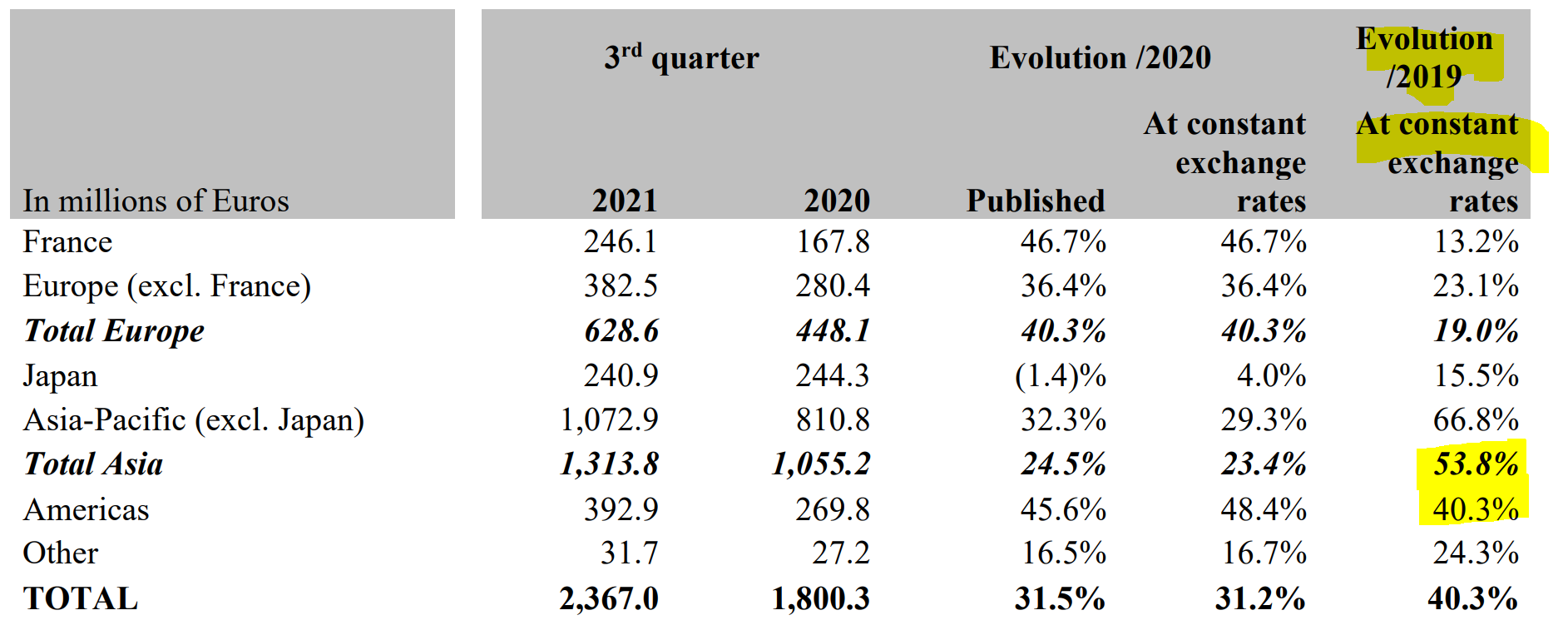

Hermes - $RMS

In the third quarter, the Group's consolidated revenue reached €2,367 million. Sales growth was outstanding at +31% at constant exchange rates compared to 2020 and reached +40% over two years. The activity benefited from an upturn in sales in Europe, an acceleration in America and a sustained dynamic in Asia.

Housing

Leading Indicator of Remodel Activity (LIRA)

“Residential remodeling continues to benefit from a strong housing market with elevated home construction and sales activity and immense house price appreciation in markets across the country,” says Carlos Martín, Project Director of the Remodeling Futures Program at the Center. “The rapid expansion of owners’ equity is likely to fuel demand for more and larger remodeling projects into next year.”

Pool Corp - $POOL

In the third quarter of 2021, net sales increased 24% to a record $1.4 billion compared to $1.1 billion in the third quarter of 2020, while base business sales grew 19%. This growth is on top of 27% growth in the third quarter of last year, bringing our year-to-date net sales growth to $1.2 billion. Our sales continued to benefit from elevated demand for outdoor living products along with favorable weather conditions.

RE/MAX National Housing Report for September - $RMAX

“This was the second-most active September for sales in 14 years, trailing only 2020, which was an outlier in many ways," said Nick Bailey, President, RE/MAX, LLC. "Plus, the expected seasonal drop in sales from August to September was half of what it usually is, indicating that buyers and sellers are still very much on the move.

The drop in home sales of 7.0% from August was less than half of the 2015-2019 average decline of 15.3%. Year over year, sales were down 4.2%.

The month-over-month Median Sales Price decline of 1.1% was one-third of the 2015-2019 average August-to-September drop of 3.4%. Year over year, the Median Sales Price is up 12.5%, with September being the fourth highest in report history. Home prices have increased year over year for 33 consecutive months.

Reflecting both the number of homes coming on the market and the velocity of sales, the 4.9% month-over-month drop in active inventory was more than double the 2015-2019 average August-to-September decline of 2.3%. Inventory was down 23.6% year-over-year. Nine months into 2021, inventory has declined month over month in all but June and July.

Zillow - $ZG

The Zillow Home Value Index (ZHVI) for the U.S. rose to $308,220 in September, up 1.6% from August. That's the second straight slowdown after monthly appreciation peaked this year at 2% in July. Monthly home value appreciation slowed from August in 44 of the 50 largest U.S. metros. Monthly growth in these markets ranged from a low of 0.4% in San Jose to 3% appreciation in Raleigh.

Despite the modest cooling, September marked the fourth-fastest monthly pace of appreciation and a record pace of yearly appreciation in Zillow data dating back to 2000. The typical U.S. home was worth 18.4% more in September 2021 than it was in September 2020, surpassing August's then-record of 17.5% year-over-year appreciation. Annual appreciation in large markets was in the double digits across all 50 major markets, ranging as high as an eye-watering 44.9% in Austin and 32.2% in Phoenix to a comparatively "sluggish" rate of 13.2% in New Orleans.

Returning inventory: The inventory shortage remains acute in much of the country, down 19.9% from this time a year ago and 37.7% below 2019 levels. However, slow, incremental growth in inventory is helping shift the scales ever so slightly in buyers' favor after hitting an all-time low in April.

Staffing

Robert Half - $RHI

Before we move on to fourth quarter guidance, let's review some of the monthly revenue trends we saw in the third quarter and so far in October, all adjusted for currency and billing days. Our temporary and consultant staffing divisions exited the third quarter with September revenues up 36% versus the prior year compared to a 34% increase for the full quarter. Revenues for the first two weeks of October were up 35% compared to the same period one year ago. Permanent placement revenues in September were up 68% versus September of 2020. This compares to a 78% increase for the full quarter. For the first three weeks in October, permanent placement revenues were up 62% compared to the same period in 2020.

The future of work increasingly includes flexible, hybrid and fully remote models, and we are uniquely positioned to benefit in this environment. We can deliver deeper skills and more price-point choices to our clients by expanding our candidate searches beyond local markets. We leverage our global office network and our advanced AI-driven technologies to deliver the best candidates for contract or permanent roles regardless of location, all while continuing to deliver the same superior customer experience our clients have come to expect.

This trend, together with elevated employee attrition rates at clients, has contributed to our staffing results recovering at a faster pace than we've experienced in the past. Our permanent placement and temporary consulting staffing segments, including blended solutions with Protiviti, have achieved cumulative sequential growth of 92% and 50%, respectively, during the first five quarters since the trough. Similar numbers for the financial crisis and the dot-com recoveries were 41% and 23%, and 45% and 31%, respectively.

The National Federation of Independent Business, NFIB, recently reported that 62% of small businesses had few or no qualified applicants for open positions and 51% had job openings that could not be filled, a 48-year record high. And we are seeing the impact of this on demand for our services on a very broad basis, spanning industries, client size, skill levels, geographies and lines of business.

Recruiter.com - $RCRT

The Bureau of Labor’s Job Openings and Labor Turnover report for August 2021 found that the number of job openings declined to 10.4 million, while hires also decreased by a total of 6.3 million.

The voluntary quit rate increased to 2.9%, reaching a new record high, while the layoffs and discharge rate was relatively stable at 0.9%. With the total number of quits increasing to 4.3 million in August it shows that the Great Resignation is upon us and that recruiters will continue to be in high demand.

The quit rates increased in accommodation and food services, wholesale trade, and state and local government education and decreased in real estate and rental and leasing.

Financials

Interactive Brokers - $IBKR

We continue to see active trading among our client base. To give a sense of this, in the third quarter of 2019, our equity volume was 41 billion shares. In the third quarter of 2020, it was 86 billion shares. This quarter, it reached 172 billion shares. Third quarter total DARTs of 2.3 million were the third highest in company history, following the first 2 quarters of this year, as existing clients continue their activity, and new clients begin to participate. Client investing confidence can also be seen in our customer margin loans, which reached a record $50.2 billion, up 67% from last year. We continue to see our clients putting their available funds to work.

First Cash - $FCFS - US Pawn Operations

Pawn receivables were up 29% at September 30, 2021 compared to the prior year, while same-store pawn receivables increased 23%, reflecting the continuing recovery in pawn balances from 2020 levels. Resulting pawn fees, which typically lag pawn receivables growth, were up 16% for the third quarter and 11% on a same-store basis, as compared to the prior-year quarter.

Retail merchandise sales for the third quarter of 2021 were up 10% compared to the prior-year quarter. On a same store-basis, retail sales increased 6% compared to the prior-year quarter.

Although pawn lending demand continues to recover, beginning same-store pawn balances entering the fourth quarter are down approximately 13% in the U.S. compared to pre-pandemic levels at the beginning of the fourth quarter of 2019. In Latin America, same-store pawn loans at the beginning of the fourth quarter are 8% below the same date in 2019.

While inventories continue to normalize to pre-pandemic levels, same-store inventory levels in both the U.S. and Latin America are still down 9% and 19%, respectively, as of September 30, 2021 compared to the same date in 2019.

“In the U.S. operating segment, pawn receivables continue to rebound from the impact of the pandemic and consumer stimulus programs with minimal impact from the federal advance child tax credit payments that began in July. Pawn receivables at the end of the third quarter were up 29% over the prior year and grew 19% over just the last three months. More importantly, pawn origination activity appears to be fully recovered, with same-store pawn loan originations over the past four weeks up 3% over the same pre-pandemic period in 2019 and same-store total customer funding (pawn loan originations plus buys) up 7% over the same period in 2019.” -CEO

Odd and Ends

Thanks for Reading and have a great Sunday!

Feel free to reach out:

@RationalResear

rationalresearch@substack.com