Facts from the Week: October 2, 2021

Facts from the Week: October 2, 2021

Highlights from $IBKR $JEF $BSET $FMCC $RDFN $BBBY $SHW $MLHR $DLTR $UNFI Financials, Gaming, Housing, Inflation, etc

Summary

Capital markets remain active with Jefferies reporting investment banking revenue up 100% lapping record revenue a year ago while Interactive Brokers reported an uptick in new accounts in September

Herman Miller reported that “demand is accelerating in the Americas Contract and Knoll segments as our customers prepare to return to their offices and adapt them for the future of work.”

Inflation and supply chain continue to be hot topics with Dollar Tree announcing price points now going up to $5

Financials

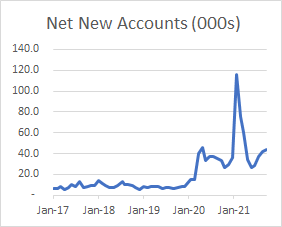

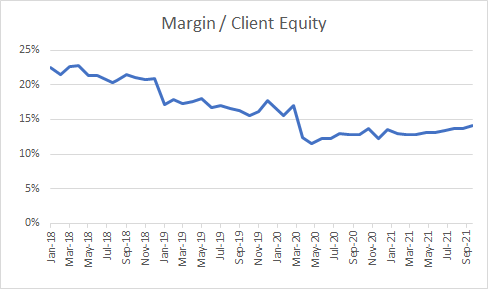

Interactive Brokers - $IBKR - September results

Jefferies - $JEF - quarter ended August 31, 2021

Net revenues of $1.65 billion, a record for a third quarter and up 19% over the prior year third quarter's then all-time record quarterly net revenues

Pre-tax income of $560 million, a record for a third quarter and up 54% over the prior year comparable quarter, and net earnings of $419 million, also a record for a third quarter and up 57% over the prior year quarter

All-time record quarterly Investment Banking net revenues of $1.18 billion, up 100% over the prior year quarter, including all-time record quarterly Advisory net revenues of $584 million, Equity Underwriting net revenues of $367 million and Debt Underwriting net revenues of $229 million, each a record for a third quarter

Quarterly combined Capital Markets net revenues of $442 million, down 32.5% over the prior year quarter, including Equities net revenues of $237 million and Fixed Income net revenues of $206 million

Gaming

Nevada Gaming Control Board

The Nevada Gaming Control Board reported August monthly gaming win of $1.17B. The mark was 57% higher than last year's level, but perhaps even more impressive, was 22% above the 2019 level. Las Vegas Strip gaming win was up 97% Y/Y to $626M and was 20% higher than the 2019 level. Downtown Vegas casinos saw a 80% jump from last year's tally while Reno casinos lagged with 19% growth. All those numbers were generated with an increase in COVID rules during the month.

Housing

Existing home sales for August - Realtor.com

"Sales slipped a bit in August as prices rose nationwide," said Lawrence Yun, NAR's chief economist. "Although there was a decline in home purchases, potential buyers are out and about searching, but much more measured about their financial limits, and simply waiting for more inventory."

Total housing inventory at the end of August totaled 1.29 million units, down 1.5% from July's supply and down 13.4% from one year ago (1.49 million). Unsold inventory sits at a 2.6-month supply at the current sales pace, unchanged from July but down from 3.0 months in August 2020.

Lumber

Bassett Furniture - $BSET

The disruptions that have permeated the furniture industry since the pandemic restart began fifteen months ago remain with us as we hit the homestretch for calendar 2021. “Business as usual” this year means raw material shortages, escalating labor and commodity costs, severely compromised logistics capabilities, and an unyielding global virus stubbornly persisting at home and in the industry’s manufacturing centers in Asia. The frustration of dealing with these dynamics is certainly wearing on the psyche of our associates and on virtually everyone else in the business. Posting consolidated revenue of $118.9 million for the quarter, an increase of 30% compared to last year and 8.7% more than 2019 did not come easily. Although there are many factors that currently encumber our financial performance, our team produced operating income of $4.5 million, 63% more than the June-August period last year and 32% more than in 2019. EPS advanced to $0.31 per share against the $0.22 recorded in 2020. We are persevering through these challenges and are squarely focused on working with our vendors to schedule adequate production to reduce our large wholesale backlog and offer higher levels of service in the near term.

Quarterly wholesale revenue grew by 32% compared to last year and by 17% to 2019. The aforementioned daily upheaval of key elements of our supply chain means we left money on the table during the period, whether that came in the form of reduced production schedules or higher incurred costs.

Moving into our fourth quarter, our backlog has continued to grow thanks to our strong three-week Labor Day retail sales event, which mirrored last year’s results. 2021 and 2020 stand as the best ever years of that holiday’s promotions. We have been able to ship above our weekly sales for the past two weeks and hope to continue that trend for the remainder of 2021.

Our retail sales have remained secure and, coupled with our fixed cost adjustments, produced a profit for corporate retail even though we are not delivering close to as much as we are writing in the stores at the moment. Gross margins for the quarter ran 290 basis points better than last year and are trending to the highest ever.

Mortgage Rates - Freddie Mac $FMCC

Redfin - $RDFN

The median home-sale price increased 13% year over year to $356,358. This was up 0.2% from the four-week period ending September 19.

Asking prices of newly listed homes were up 12% from the same time a year ago to a median of $361,250, an all-time high. Asking prices have been on the rise throughout the month of September, in a typical late-summer seasonal uptick.

Pending home sales were up 4% year over year, the smallest year-over-year increase since June of 2020.

New listings of homes for sale were down 8% from a year earlier. New listings have been below 2020 levels since the four-week period ending August 22.

Active listings (the number of homes listed for sale at any point during the period) fell 22% from 2020.

Bed Bath and Beyond - $BBBY

Comparable Sales decline of (1)% versus Q2 2020 primarily driven by slower than expected traffic trends in August across stores and digital

F3Q21 guidance: On a Comparable Sales basis, the Company expects to be approximately flat compared to the prior year period.

“While our results this quarter were below expectations, we remain confident in our multi-year transformation. Following solid growth in June, we saw unexpected, external disruptive forces towards the end of the quarter that impacted our outcome. In August, the final and largest month of our second fiscal period, traffic slowed significantly and, therefore, sales did not materialize as we had anticipated. As COVID-19 fears re-emerged amid the on-going Delta variant, we experienced a challenging environment. This was particularly evident in large, key states such as Florida, Texas and California, which represent a substantial portion of our sales. Furthermore, unprecedented supply chain challenges have been impacting the industry pervasively, and we saw steeper cost inflation escalating by month, especially later in the quarter, beyond the significant increases that we had already anticipated. This outpaced our plans to offset these headwinds. These factors impacted sales and gross margin." -CEO

From July to August, traffic trends evolved in this state and worsened by double-digit percentages. The rapid decline in traffic was particularly detrimental for us given the inclusion and significance of August in our fiscal quarter versus our competitors. We are cognizant of comparisons to our peers who are on a July end reporting cycle. As a proxy, our comparable sales grew an estimated 24% based on May, June, July, further highlighting the importance of the trading month of August on our Q2 performance.

So far in the month of September, we have not seen an improvement from the challenging traffic and sales trends we experienced in August. Having said that, similar to last quarter, the final month of this quarter, November, is the largest and most impactful.

Sherwin Williams - $SHW

"As demand remains robust across our pro architectural and industrial end markets, we continue to make investments in our strategic growth initiatives, including bringing 50 million gallons of additional architectural production capacity online over the next two quarters," said Chairman, President and Chief Executive Officer, John G. Morikis. "At the same time, the persistent and industry-wide raw material availability constraints and pricing inflation we have previously reported have worsened, and we do not expect to see improved supply or lower raw material pricing in our fourth quarter as anticipated. As a result of these headwinds, we are narrowing our third quarter sales expectations and establishing third quarter earnings guidance. For the full year, we now expect sales to be up by a high single digit percentage and adjusted diluted net income per share guidance to be $8.45 at the midpoint of the range.

Herman Miller - $MLHR

Strong demand and the Knoll acquisition drove quarterly orders of $916.5 million, an increase of 64.8% compared to the prior year period, up 34.5%* organically

Our Global Retail business maintained its strong momentum with sales and orders up 30.7% and 22.2% over the prior year period, respectively. This is on top of strong growth this time last year, with orders growing 90% on a two year stack. We continue to outpace the US home furnishings industry with our growth numbers.

We continue to experience strong momentum in our Global Retail and International Contract segments. Demand is accelerating in the Americas Contract and Knoll segments as our customers prepare to return to their offices and adapt them for the future of work. Order levels increased over the prior year for all reportable segments. We believe that this positive order demand is an indicator of the strength of our business strategy, and underscores our confidence in the future as we lead the industry in redefining modern design as MillerKnoll.

Our second quarter fiscal 2022 guidance includes the full impact of Knoll for the quarter. We expect sales in the second quarter of fiscal 2022 to range between $1,025 million and $1,065 million. The mid-point of this range implies a revenue increase of 67% compared to the same quarter last fiscal year on a reported basis and 12% on an organic basis, excluding the impact of the Knoll acquisition and foreign currency translation.

Inflation

Bassett Furniture:

We instituted our fourth general price increase of the year on September 13th. The pace of incoming increases from our suppliers has subsided somewhat from earlier in the year but remains significant. Unfortunately, we have not been able to enact price increases on our goods as fast as we have incurred them from our material providers. The most glaring example is the escalation in ocean freight that has quintupled in the past twelve months, which affects not only our imported products but many of the components that are used in our domestic production. During the quarter, the rising prices on container freight ramped up as the availability of space on the giant vessels that move goods from Asia to the U.S. declined. In effect, the shipping companies are conducting daily auctions for space on their vessels, causing container prices to fluctuate wildly from day to day. This was driven, of course, by the fact that the aggregate demand for goods to move into the U.S. has consistently outstripped the supply of cargo space available to move it for most of 2021. Recent demand of containers has been somewhat tempered by Vietnam’s enactment of Martial Law, which has shut down all manufacturing activity in the country in an attempt to curb the Delta virus. Our information tells us that it will be late October before production fully returns, which will begin to affect our shipments in late Q4 and into fiscal 2022. -CEO

Dollar Tree - $DLTR

today announced that, based on positive customer reaction and the success of its new Combo and Dollar Tree Plus store formats, the Company plans to begin adding new price points above $1 across all Dollar Tree Plus stores and will begin testing additional price points above $1 in selected legacy Dollar Tree stores.

Dollar Tree has already announced that it is on track in 2021 to have 500 Dollar Tree Plus stores by fiscal year-end – offering an assortment of value priced $1, $3, and $5 products. Another 1,500 stores are planned for fiscal 2022, and at least 5,000 Dollar Tree Plus stores are expected by the end of fiscal 2024.

United Natural Foods - $UNFI

I think the way we think about '22, we're including about 1% inflation for the year. We know the situation we're in right now. But as it relates to a full year, we think we're going to on par come back to roughly a 1% for the year. -CFO

Sherwin Williams

"Our suppliers are now reporting that the impacts of Hurricane Ida are more severe and will be longer lasting than initially thought. Production of several key resins, additives and solvents, expected to resume by late September, has been pushed out. We now expect raw material availability issues to negatively impact our consolidated sales by a high-single digit percentage in the fourth quarter. This follows the high-single digit impact in the third quarter we previously communicated. We will continue to partner closely with our suppliers to improve supply while employing all of our assets to reduce the impact on our customers. We are confident the majority of sales delayed by these conditions will be recovered over future quarters as raw material availability improves.

"In addition to the significant supply challenges, raw material pricing remains highly elevated, and we are increasing our full-year raw material inflation outlook to be up a high-teens percentage compared to last year. We continue to combat these elevated costs with pricing actions across all of our businesses. We are maintaining staffing in our manufacturing facilities to ensure we meet the demand as quickly as raw material availability issues subside. While maintaining these costs puts additional pressure on our third and fourth quarter earnings, we are committed to providing the resources necessary to drive our customers' success.

Cotton Futures

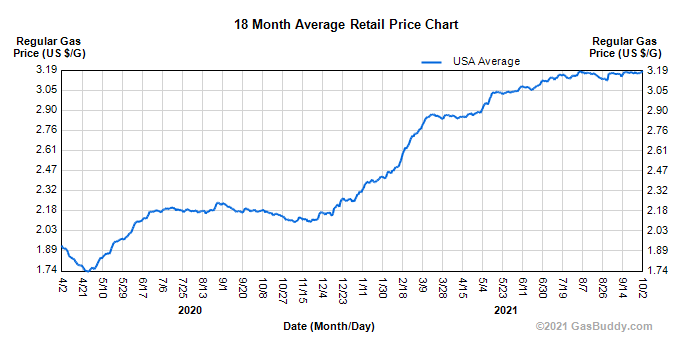

Gas Prices - Gas Buddy

Odds and Ends

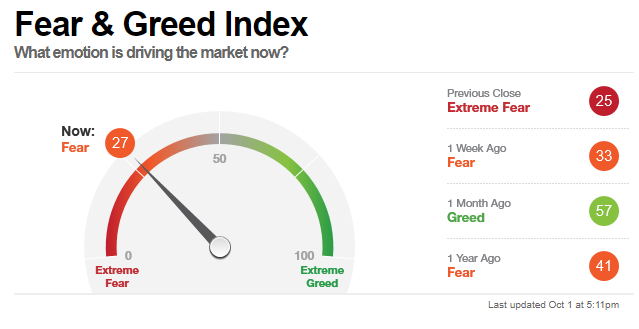

Fear and Greed Index - CNN

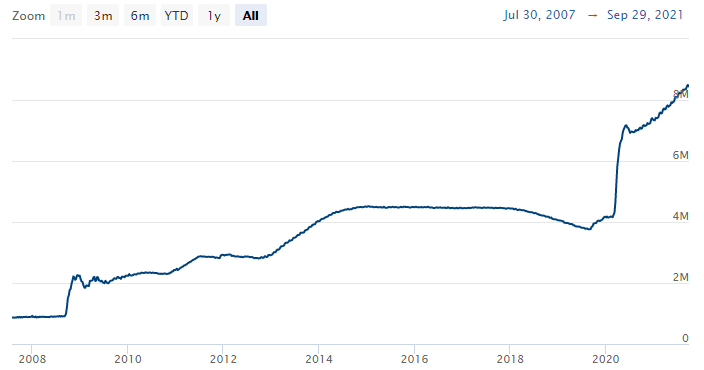

US Federal Reserve Balance Sheet

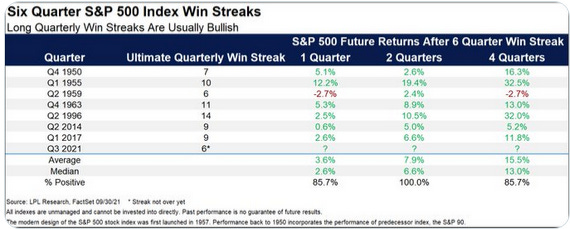

Barring an extreme finish today, the S&P 500 is about to be up six quarters in a row. Remarkably, the next quarter has been lower only once and perhaps even more incredibly, two quarters later stocks have never been lower. A year later? The market is up 15.5% on average. Yet another clue, says LPL, that we are in a secular bull market and the surprises will be to the upside. - JP Morgan

Thanks for reading and have a great weekend!

Feel free to reach out:

@RationalResear

rationalresearch@substack.com