ODP Corp - $ODP: remaining distribution biz is a good biz trading for ~1x EBITDA

Sum-of-parts compelling with upside option in Varis

Summary

Ick investing means taking a special analytical interest in stocks that inspire a first reaction of “ick.” I tend to become interested in stocks that by their very names or circumstances inspire an unwillingness – and an “ick” accompanied by a wrinkle of the nose – on the part of most investors to delve any further. In all probability, such stocks will prove fertile ground for the rare neglected deep value situations that could provide significant returns with minimal risk, and minimal correlation with the broad market. Occasionally, well-known stocks fall into the “ick” category, and it is at those times that I become interested. - Michael Burry

The quote above from Michael Burry summarizes a typical first reaction to hearing the name ODP Corp or Office Depot. However, after a little digging, the post-transaction(s) ODP distribution business looks like a good business at a very attractive multiple with substantial downside protection.

To summarize, ODP could be sitting on $32/share of cash with the stock below $40 leaving $8/share or $408m market value for the remaining Business Solutions Division which did $287m of normalized EBITDA in 2019 (~1.5x EBITDA) and contains an compelling upside option in Varis.

Timeline:

January 11, 2021: Sycamore bids $40 for ODP Corp

Source: 11/3/21 10Q: On January 11, 2021, we received a proposal from USR Parent, Inc., the parent company of Staples Inc. and a portfolio company of Sycamore Partners, to acquire 100% of our issued and outstanding stock for $40.00 per share in cash (the “January Proposal”).

June 4, 2021: Sycamore bids $1bn for ODP’s retail business

June 29, 2021: Compucom business is reclassified as “held for sale”

Source 10Q: The CompuCom disposal group has met the accounting criteria to be classified as held for sale as of June 29, 2021 and is presented as discontinued operations starting in the third quarter of 2021.

November 5, 2021: Sycamore reaffirms $1bn bid for ODP’s retail business

Source: 11/8/21 SC TO-C: November 5, 2021—USR Parent, Inc. (“Staples”) today reaffirmed its June 4, 2021 proposal to The ODP Corporation (together with its subsidiaries, the “Company”) to acquire the Company’s consumer business for a cash purchase price of $1.0 billion. This proposal was formally delivered to the Company on June 4, 2021 and remains unchanged.

Sum of the Parts:

***ODP had 51.573m shares out as of 10/27/21 (and management has been shrinking the share could with buy-backs, more on that later)***

Cash Balance:

ODP has net cash of $400m or $7.75 per share at 9/25/21 ($753m cash and $353m debt)

Worth noting that ODP has been generating substantial free cash flow with adjusted free cash flow of $474m in 2020 and adj EBITDA of $491m in 2020.

Retail business:

$1bn bid from staples reaffirmed 11/5/21, this is worth $19.39/share

$1bn values the retail business at 2.5x trailing EBITDA. One could argue this is a low multiple given the retail business 10% EBITDA margins and sales growth per store. Additionally, ODP’s retail assets are strategic to Sycamore if they plan to take Staples public. And as a comparison, BBBY has traded in a range of 3-12x EBITDA over the past 3 years.

Compucom:

Management is in the process of selling this asset. Estimating ODP gets $250m for Compucom, which is roughly 0.3x trailing sales and 6x EBITDA. ODP paid $937 for Compucom on 11/8/17. Compucom is “held for sale” and management hopes to announce a transaction before year end. $250m is worth $4.85/share.

11/3/21 earnings call: “With respect to CompuCom, the previously disclosed sale process continues to progress. We are working towards announcing the transaction before the end of the year, but there can be no assurance that we will do so.”

Headquarters Real Estate

ODP purchased its corporate headquarters in Boca Raton, Florida in 2017 for $132m. The value has likely increased since then, but conservatively using $132m would another $2.56 per share. Since I have not heard management discuss selling this asset, I will not included it.

Source: https://www.sun-sentinel.com/business/fl-bz-office-depot-buys-headquarters-20170811-story.html

So the sum of the current cash balance, sale of retail, and sale of compucom 7.75 + 19.39 + 4.85 = $31.99 per share of cash. This does not include the $2.56/share+ for the owned real estate. ODP stock is below $40 today (11/16/21) at $39.88.

So for the remaining $7.89/share i.e. $407m enterprise value you get the Business Solutions Division (and the real estate).

Business Solutions Division (BSD)

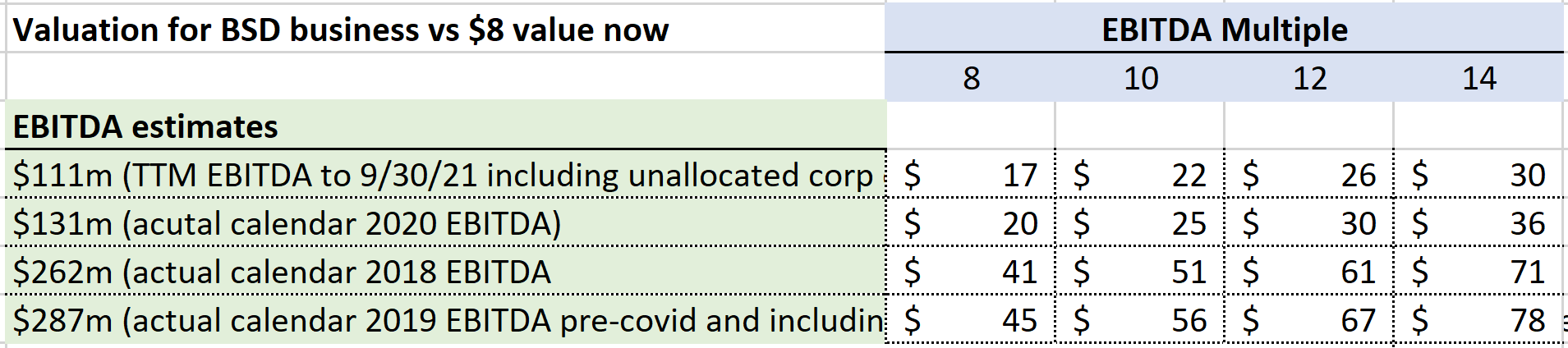

Looking at pre-covid trends, BSD did $287m of EBITDA in 2019 and $262m in 2018. Note this includes a proportionate amount of unallocated corporate expenses in an effort to represent what BSD could look like as a stand-alone business.

$407m enterprise value / $280m normalized EBITDA = 1.45x EBITDA

And one could argue that BSD is a pretty good business:

BSD can deliver next-day to 98.5% of the US Population

Source: 10K 2/25/21: “With our network of DCs, crossdocks, and vehicles, we are capable of providing next-day delivery services for approximately 98.5% of the population in the United States.”

Valuable supply chain assets including 71 DCs and 1000 vehicles. These assets may be more valuable than ever today given supply chain disruption and need for fast delivery:

Source 10K: We continue to invest in our supply chain network, focusing on further enhancing our capabilities, increasing efficiency and lowering our costs. For example, we have grown our private fleet of transportation vehicles and introduced automated technology and robotics into our DCs and crossdock facilities. These investments position us to pursue opportunities beyond our traditional business, including utilizing our supply chain as a logistics service for third parties, including our customers.

Generates a lot of cash flow (nearly $5/share pre-covid) and capex is modest compared to EBITDA

Steady revenue, EBITDA, and free cash flow as shown below. Worth noting:

Shift to digital didn’t kill BSD

Amazon didn’t kill BSD

Covid work-from-home-hybrid didn’t kill BSD (still profitable every quarter of 2020 and 2021)

Still generating positive free cash flow despite Covid pressures. On a covid-depressed trailing-12-months, BSD did $1.42 in FCF, so trading at 5.6x depressed cash flow.

BSD should have a nice tailwind from here as the economy reopens, people go back to the office and back to school. Employees returning to the office has been delayed, but seems like it should continue to incrementally increase from current levels.

One recent anecdote: “Google CEO says offices filling back up” from 10/18/21: https://www.cnbc.com/2021/10/18/google-ceo-sundar-pichai-says-offices-are-filling-back-up-.html

And management has noted they expect BSD to return to pre-covid levels either in 2022 or get to the 2019 “run-rate” in 2022:

“It's too early to tell whether the trends back to 2019 occur in 2022 or we start to see that pace begin in 2022 and continue on in years there.” -CFO 11/3/21

What could BSD be worth?

Comparable distribution businesses:

Sycamore/Staples bought Essendant, a distributor of office supplies, for 10.3x trailing EBITDA in January 2019 worth $1bn LINK

Source: Proxy 9/24/18: “a multiple of 10.3 times the Company’s last 12 months (as of June 30, 2018) adjusted EBITDA.”

Fastenal 12.5 to 22x EBITDA, 3-5x sales

Grainger 10-14x EBITDA, 1.4-2.0x sales

Others include Pool Corp, Cintas, MSC Industrial, Genuine Parts, HD Supply, etc

Below are potential EBITDA levels and multiples for the BSD business which currently has an implied market value of $7.88/share. Note that Fastenal and Grainger have higher margins which might warrant higher multiples.

*EBITDA includes proportionate amount of “unallocated” corporate expenses based on revenue split to approximate what BSD would look like as a standalone business

So add the $32 of cash (or your estimate of cash) to your estimate of the BSD value to come to a sum-of-the parts.

Free Call Option - Varis

ODP management has not said much about Varis yet, but they have hired some excellent talent that might foreshadow a big opportunity. Varis is a “digital procurement platform” and in February 2021, ODP announced they hired Prentis Wilson, who built Amazon Business to $10bn of sales, to lead the Varis business LINK:

Wilson has a strong track record of successfully building large-scale, disruptive, B2B technology businesses. He spent almost eight years at Amazon.com, Inc., where he launched Amazon Business and grew it to over $10 billion in annual sales. Prior to joining Amazon, he held senior operations and B2B procurement roles at Cisco Systems, Inc. and Honeywell International, Inc. Most recently, he was the President of Boxed.com, a wholesale technology start-up.

Additionally, Terry Leeper joined ODP in July 2020 as Chief Technology Officer from Amazon and Microsoft: LINK

Leeper previously held executive positions at Amazon and Microsoft. He most recently served as Head of Product and Tech of Amazon Business for six years, prior to which he was Director of Software Development for Amazon’s Retail Systems Platforms. Before Amazon, Leeper was with Microsoft for 12 years, where he held the positions of Director Platform Strategy while living in the U.K., and Director of Developer Division while living in China.

More recently, a significant amount of talent has joined Varis. The Varis website shows 6 of the 9 executives at Varis have joined from Amazon: https://www.govaris.com/about-us

Chief Commercial Officer: Previously at Amazon for seven years in executive General Management roles, including launching the B2B division of Amazon Devices & Digital and a founding member of the Amazon Business leadership team.

SVP Public Sector: Most recently, Director, Public Sector, for Amazon Business, where she was responsible for scaling Amazon’s B2B business to support sourcing and procurement requirements, including regulatory compliance, across Federal, State and local customers.

SVP Strategy: Prior to joining Varis, spent five years at Amazon, most recently as General Manager responsible for Amazon Flex in North America along with international expansion. She also served as Director, Amazon Business, where she led Product and Engineering for Amazon Business International expansion and growth.

SVP Payments: Most recently, he worked as VP of Amazon Capital Services, Inc. and Director of World-wide B2B Payments, where he drove the Business Payments and Seller Lending businesses across all operating Amazon marketplaces.

Director of Operations: was Sr. Manager, Amazon Business – Business Operations and Program Manager, Amazon Business Product Tech at Amazon.

A search of Varis LinkedIn page shows that of the 100 people listing Varis as their current employer, 17 list Amazon as a former employer and many from the Amazon Business segment.

One observation is that this much top-talent does not leave Amazon to join ODP Corp unless something good is happening. And since the BSD business is trading at less than 2x normalized EBITDA, the market does not seem to be pricing in any upside related to Varis.

Varis Background:

Varis is a digital procurement platform and the company acquired BuyerQuest in January 2021 to accelerate these efforts and in February 2021 announced a partnership with Microsoft in February 2021 to be on the Dynamics 365 platform:

Source 11/3/21 10Q: As part of this transformation, we are evolving our B2B business and developing a new digital platform technology business, which has been named Varis, and aims to transform the B2B procurement and sourcing industry by filling the growing demand for a modern, trusted, digital B2B platform. On January 29, 2021, in connection with our development efforts in this area, we acquired BuyerQuest, a business services software company with an eProcurement platform for approximately $71 million, subject to customary post-closing adjustments.

From 2/24/21 earnings call:

So from a BuyerQuest perspective, it obviously accelerates our ability to -- as we build out our digital platform. The digital platform has a Procure-to-Pay piece that has a supply chain piece and e-commerce piece. And all that is obviously addresses the $8 trillion market.

The BuyerQuest acquisition, Jack and his team have a world class product. It's rated very high, I believe, by Gartner. What it has done is it accelerate our ability to really get into that Procure-to-Pay marketplace, and we think that's a huge opportunity, especially as we have announced the relationship with Microsoft.

Microsoft is excited to partner with this from both an Azure perspective, we thank them for that support as well as the ability to move into that Procure-to-Pay -- be the Procure-to-Pay element of their Dynamics 365 ERP package. So obviously, we think that's a huge opportunity for both companies, especially being on that front-end at procure to pay, more to come on that because, obviously, once we have that for Procure-to-Pay platform in Dynamics 365, there's a huge opportunity of having all those customers have the ability to buy on a marketplace or a platform to go off and buy. And more to come on that Investor Day. But obviously, that's a huge market opportunity in the future, partnering with Microsoft. -CEO Gerry Smith

Share Buy Back

Management has stepped up the share buy back since June 2021. The share count at 10/27/21 was down 3.3% from 7/28/21:

ODP reported $474m of adjusted free cash flow in 2020 and $310m in 2019 in addition to the $400m of net cash on the balance sheet, so it would seem ODP is in a good position to get more aggressive on the buy back with the share price below $40. A tender offer at these prices could be significantly accretive particularly as ODP will have more cash coming in from the pending sale of Compucom.

People

HG Vora is an activist investor, owns 9.5% of ODP, and joined the board in January 2021:

“ODP has made significant progress in pivoting its business to a compelling B2B platform and is committed to delivering superior shareholder value by continuing its growth initiatives and exploring potential strategic transactions. I look forward to working with my fellow ODP directors as the Company continues its evolution.” - HG Vora, January 2021

Gerry Smith has been CEO since 2017. He owns 602k shares worth ~$24m.

Prior to joining the Company and since 2006, Mr. Smith was at Lenovo and previously served as Lenovo’s Executive Vice President and Chief Operating Officer since 2016 where he was responsible for all operations across Lenovo’s global product portfolio. Prior to assuming this role, also in 2016, Mr. Smith was Executive Vice President and President, Data Center Group.

See above on key hires at Varis

Also… a spin-off

Management has announced a tax-free spinoff to separate the BSD and Retail Business in the first half of 2022. So if ODP does not take the bid from Sycamore, potentially the market will be able to value the two separate businesses appropriately. And note that Varis stays with the BSD business (as will the current CEO). From the 11/3/21 earnings release:

The Company continues to make progress on its plans to separate ODP into two, independent, publicly-traded companies, making advancements in all areas of the separation including organizational structure, operating and supply chain mechanics, IT support, and on the anticipated market-based commercial agreements between the companies. During the quarter, the Company announced the selection of the chief executive officers of both companies, which would become effective upon completion of the spin-off, as well as the company names for each of the two companies.

It was announced that Gerry Smith will continue to serve as the CEO of the ODP Corporation following the separation. As a leading supplier of B2B solutions serving small, medium and enterprise level companies, The ODP Corporation will consist of several operating companies, including the contract sales channel of ODP’s current Business Solutions Division, which will be renamed ODP Business Solutions, and ODP’s newly formed B2B digital platform technology business, which will be named Varis. ODP Business Solutions and Varis will be owned by ODP, but operated as separate businesses. ODP will also continue to own the global sourcing operations and other sourcing, supply chain and logistics assets.

The separation is expected to allow The ODP Corporation and Office Depot, Inc., to pursue unique market opportunities and growth strategies, improving value for all stakeholders. While the companies will be separate, independent companies, it is anticipated that they will share commercial agreements to allow them to continue to leverage scale benefits in such areas as product sourcing and supply chain. The expected timing remains the same as previously announced, with estimated completion in the first half of 2022.

So the spin-off provides some additional downside protection assuming ODP does not accept the Sycamore bid for retail. Presumably the market would be better equiped to value the retail and distribution businesses separately. This is in addition to Sycamore having bid $40 for all of ODP in January (stock at $40 now), ODP generating cash, and ODP having $400m of net cash on the balance sheet. Downside Protection

Why does this opportunity exist?

“ick” factor

mis-perceived as a brick and mortar retailer

sum-of-parts takes some work

Varis has not been talked much about by management, and is not well known to investors

RISKS:

Management does not execute on the opportunities at hand, Sycamore walks away and the spin-off is unsuccessful

Supply chain costs and inflation as noted on recent earnings call

Upcoming results are uninspiring as people are slow to return to the office

FTC Risk

Counterpoint on FTC Risk: from 11/8/21 SC TO-C: “In November 2020, Staples filed the necessary governmental approvals with the Federal Trade Commission to acquire the Company, and has made substantial progress responding to the government’s data requests and inquiries in connection therewith. With the Company’s full cooperation, Staples is confident that the parties will be able to expeditiously obtain the necessary antitrust approvals for the proposed acquisition of the Company’s consumer business.”

Retail and Distribution are intertwined and separating the two makes each less profitable

Significant passive ownership makes it difficult to maximize shareholder value

Every risk that goes with public market investing and investing in general

Disclaimer

This is not a recommendation to buy or sell and is for discussion purposes only. Do you own research. I am under no obligation to follow-up as events unfold.

Thanks for reading and please reach out with any insights:

rationalresearch@substack.com

@RationalResear

Appreciate the write up, great analysis. I'm not sure about your share count figure of 51.5m.

I have weighted shares outstanding (dilute) as 56m per Note 7 of FY21Q3 10Q pg 21 .

Great write-up. ODP is staggeringly cheap. A no-brainer investment in my opinion.