$TUESQ 🔜 $TUES = Tuesday Morning

Repositioned retailer trading at less than 3x cash flow with tailwinds, a solid balance sheet, and improved executive team. Equity potentially mis-priced.

Summary

Tuesday Morning announced on December 23, 2020 that the company received confirmation to exit bankruptcy by month end. $TUES is now well positioned for success. Based on company projections, TUES trading at less than 3x cash flow with a net-cash balance sheet and a significantly improved cost structure.

Company projections seem realistic as cost cuts and rent reductions have already been implemented as disclosed in monthly operating reports. Filing bankruptcy gave $TUESQ a wonderful opportunity to close under-performing stores and reduce rent expense on the remaining stores. TUES retained its 490 best stores which have produced solid results over the past few years while closing 199 underperforming stores. Of the 490 remaining stores, leases have been renegotiated on 386 taking rent expense from $118m to a $67m run rate. The $51m rent expense savings is significant relative to the $20m of EBITDA $TUES did in F19.

The board is comprised of executives with strong retail experience. Four new board members should position the company for future success including Chairman of $HIBB/Former CFO of $TSCO.

Potential up-listing, coming vaccine, easy comparisons, and improved inventory flow are positive events on the horizon.

Note that current share purchases MIGHT be able to participate in the upcoming rights offering at $1.10 but please verify to you own satisfaction. Recent 8K has additional info including “The Company currently anticipates the “rights offering/exchange determination date” will be the close of business on January 4, 2021”: LINK

Tuesday Morning was founded in 1975 and currently operates 490 stores averaging 12k square feet offering a treasure hunt experience primarily in home goods.

People:

CEO and Chairman: Steven Becker has been CEO since 2015 and owns 5.5% of shares as of 9/30/19. Becker is a former fund manager though he has retail experience having served on the board of Hot Topic and Ruby Tuesday amongst other public company boards. However, Becker does not have an operational background and it could be a positive if the company brought in an experience CEO. Becker had been buying stock in the open market up until the end of 2019:

Chief Merchant: Paul Metcalf assumed the role of acting chief merchant on December 9th, 2019 after consulting TUES since April 2019. He has 30 years of experience from $BURL and $TJX plus others:

Mr. Metcalf has over 30 years of retail experience. Prior to his role at Tuesday Morning, he was the Executive Vice President and Chief Merchandising Officer at Burlington Stores, Inc. While there, Mr. Metcalf successfully led the transformation of the merchant organization and helped to take the company public in 2013 (Mr. Metcalf is credited with BURL’s shift to off-price).

Prior to his role at Burlington Stores, Inc., Mr. Metcalf was a senior leader in the merchant organization for The TJX Companies, Inc where he was one of 3 senior merchants.

Most recently Mr. Metcalf led a similar successful merchandise turnaround at the off-price retailer, Gabriel Brothers prior to its sale to Warburg Pincus.

He began his career with May Department Stores where he held a variety of positions within the merchant organization.

Importantly, over the past 18 months Paul has hired 11 new merchants primarily trained at Ross, TJX, and Burlington

Board members (Source: docket #1879):

Anthony Crudele: New board member, he is Chairman at Hibbett Sports and was CFO of Tractor Supply from 2005 to 2017

Doug Dossey: New member from Tensile Partners (lender to company)

W. Paul Jones: New member, former CEO of Payless Shoes, on board at JC Penney

John Lewis: New member, founder of Osmium Partners, LLC who will be major shareholder after the $40m rights offering

Frank Hamlin: Chief Customer officer of Gamestop, on board since April 2014

Reuben Slone: VP of Supply Chain at Advance Auto Parts, on board since June 2019

Sherry Smith: former CFO of SUPERVALU, on board since April 2014

Richard Willis: CEO of Pharmaca Integrative Pharmacies, on board since 2012

Timeline

Fiscal Year 2019 (ended June 2019) $TUES reported $20m of EBITDA and positive comps

December 2019: Paul Metcalf assumed role of Acting Chief Merchant

May 2020: Tuesday Morning filed for Chapter 11 Bankruptcy protection

May to September 2020: $TUES closed unproductive stores: 490 stores on 9/30/20 from 707 on 9/30/19 and restructured leases on most of the remaining stores

December 2020: Sold real estate for $70m which was $10m more than expected (Dallas News):

“On December 7, 2020, the Company and certain subsidiaries entered into a purchase and sale agreement with PBV – 14303 Inwood, LP, pursuant to which the New Purchaser agreed to purchase the Company’s Dallas headquarters and warehouse facilities for an aggregate purchase price of $70.25 million.” (Source 8-K LINK)

December 22, 2020: Confirmation hearing for the bankruptcy judge to approve TUES emergence from bankruptcy

December 23, 2020: “Tuesday Morning and certain of its subsidiaries today announced that the U.S. Bankruptcy Court for the Northern District of Texas has confirmed the Company’s Plan of Reorganization (the “Plan”). As a result, Tuesday Morning expects to successfully emerge from Chapter 11 protection by the end of December after it has satisfied the conditions to the effectiveness of the Plan.” LINK

December 31, 2020: $TUES should emerge from bankruptcy LINK

January 2021: Osmium Partners, LLC will backstop a $40 million rights offering at $1.10/share (Source LINK)

“The Company currently anticipates the “rights offering/exchange determination date” will be the close of business on January 4, 2021.”

“The exercise price per share of the Eligible Offeree Rights Offering Common Stock acquired pursuant to an Eligible Offeree Share Purchase Right shall be $1.10 per share (“Exercise Price”).” (Source: Amended disclosure statement 11/13/20)

Repositioned Stores: $TUES used BK to close 1/3 of stores and reduce lease costs on remainder

Filing bankruptcy gave TUES a perfect opportunity to shed the bottom 199 stores and reposition the remaining 490 stores, which were already pretty good stores, with even better lease terms.

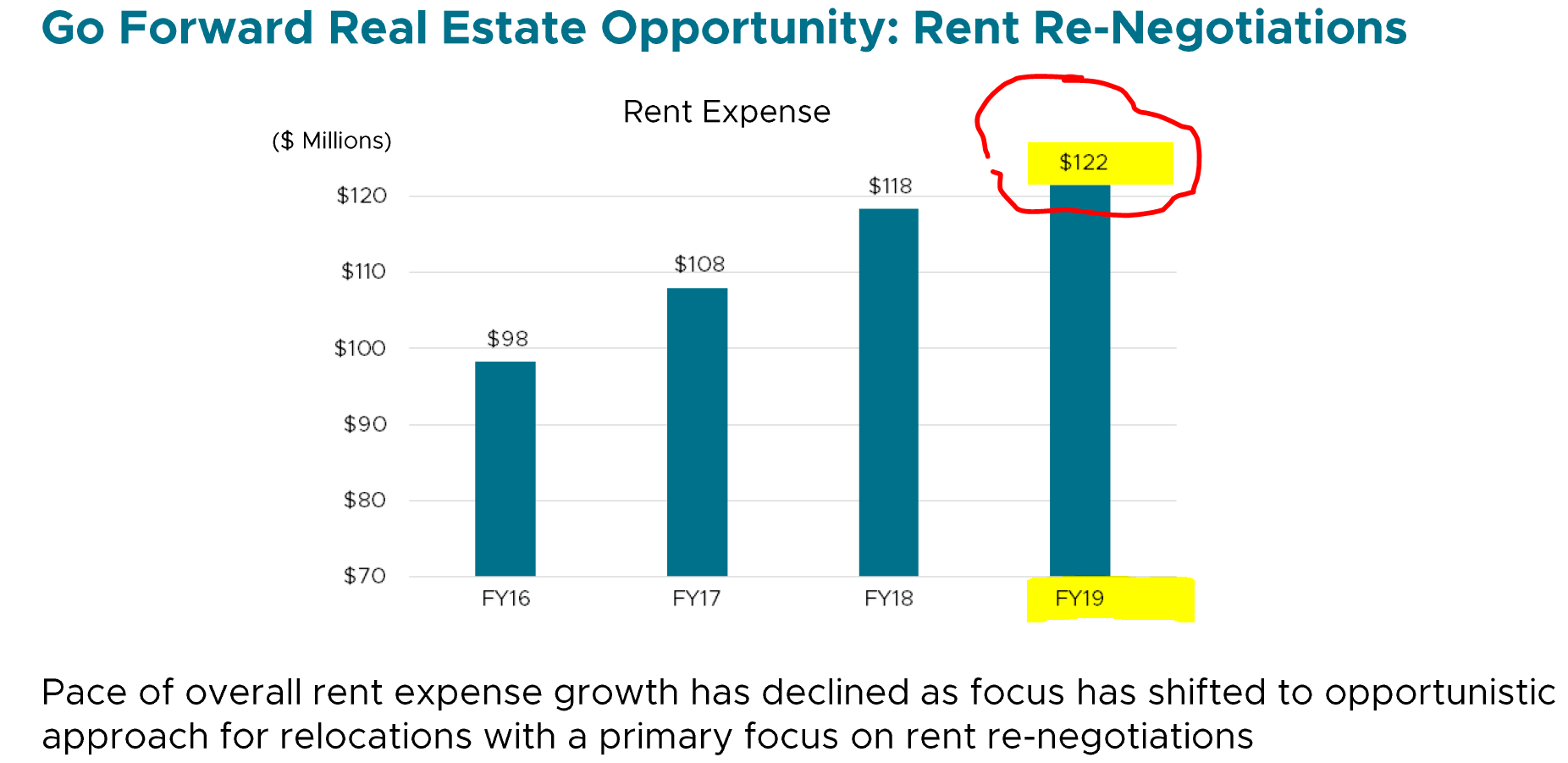

Pre-Covid rent expense had been escalating and management was focused on rent reductions. Rent expense was $122m in Fiscal 2019 (year ended June 2019). Below is from TUES’ presentation in October 2019 which shows rent escalation issues:

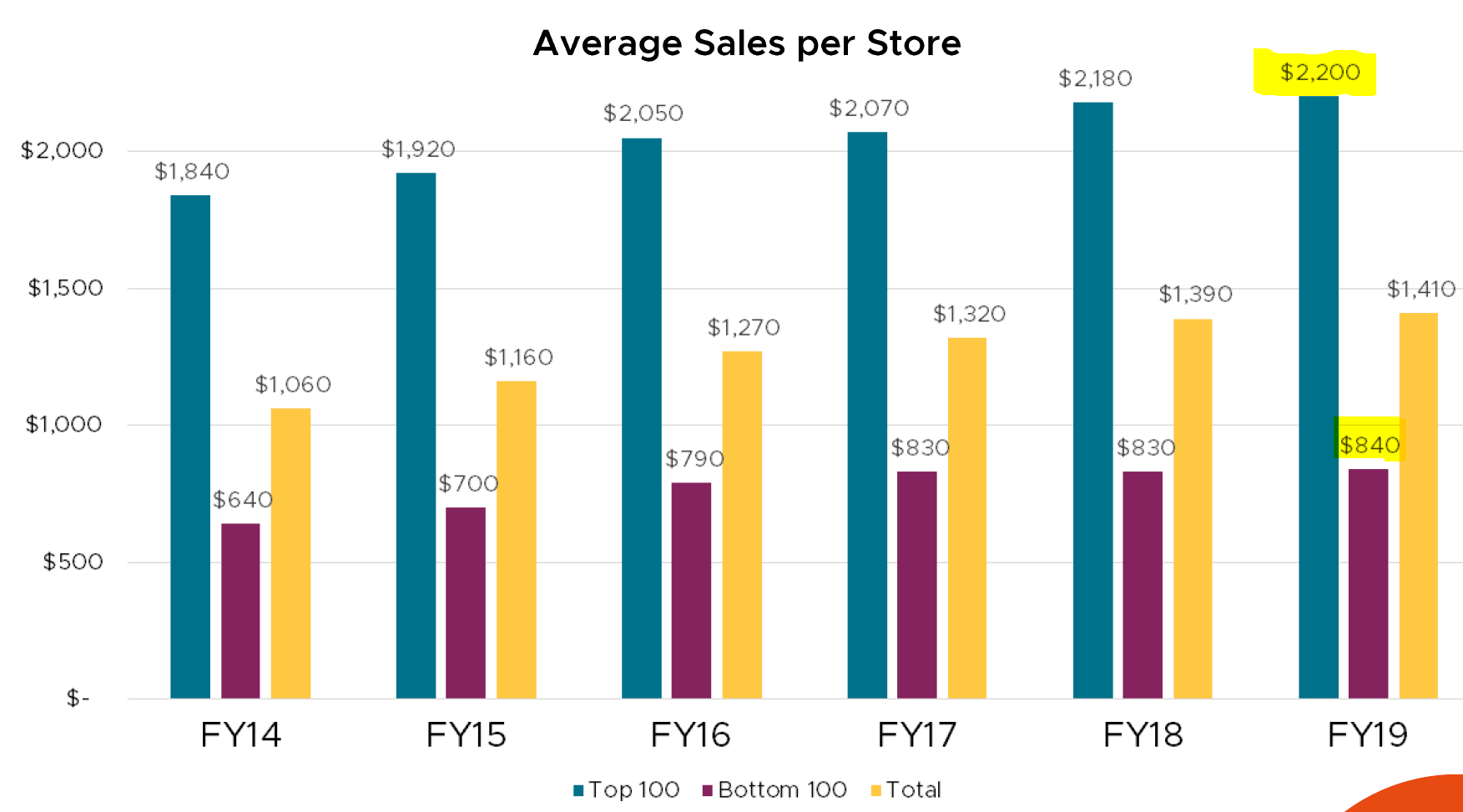

Additionally, the discrepancy between the best 100 stores and bottom 100 stores was significant. According to the company, the remaining stores average 50% higher revenue than the stores that were closed.

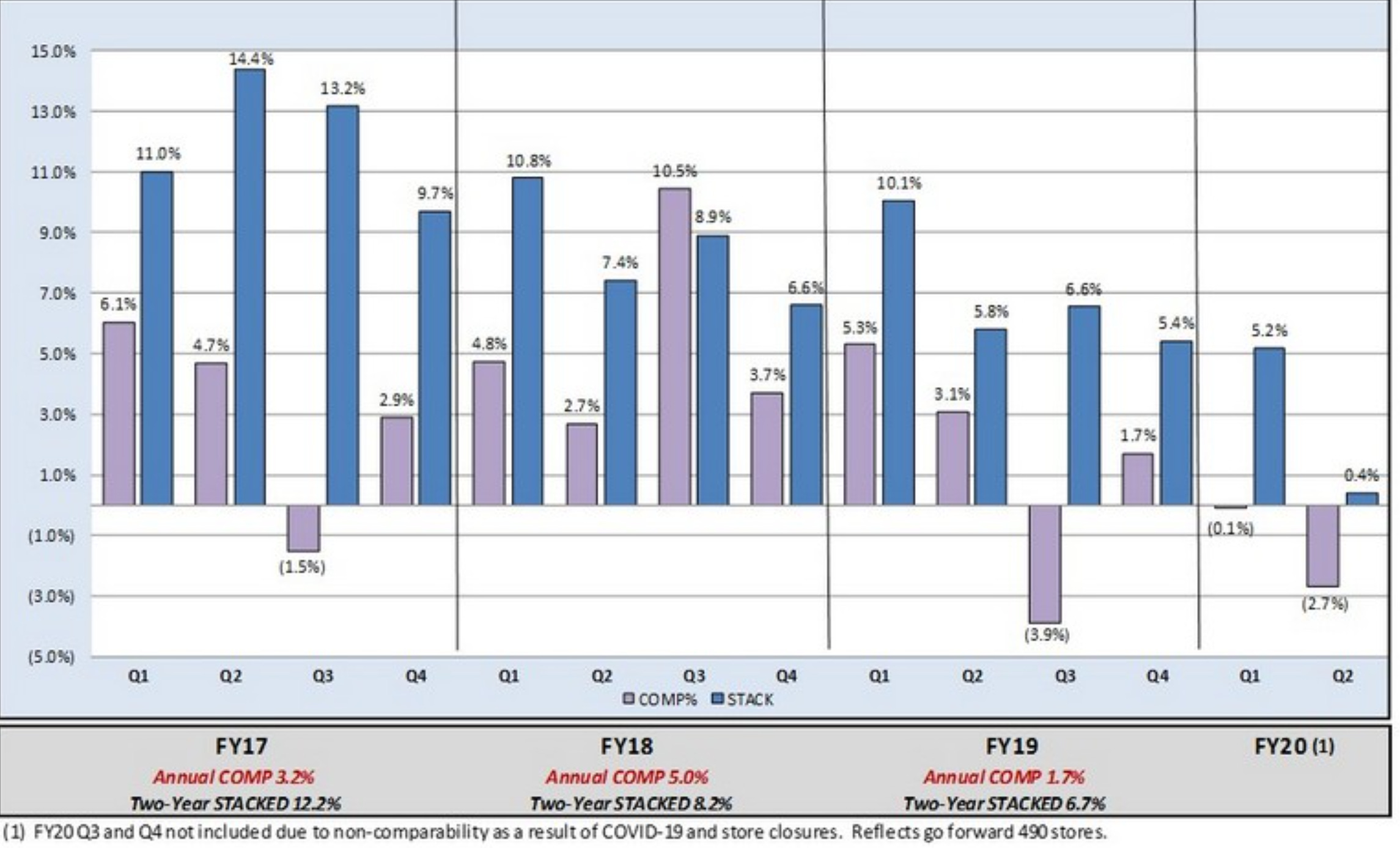

And despite the underperforming stores, comps had been positive in 10 of the 14 quarters to December 2019. This is relatively good for a brick-and-mortar retailer and shows there is appetite for the brand which has 45 years of history and a loyal following.

Filing bankruptcy gave $TUES a great opportunity to shed the bottom 199 stores and reposition the remaining 490 stores (which were already relatively good stores) with even better lease terms.

Of the remaining 490 stores, leases on 386 have been renegotiated. As part of the BK procedures, TUES must provide monthly operating reports which show average rent and lease payments over the past 4 months of August thru November 2020 of $5.6m per month which annualizes to $67m.

So TUES is already benefiting from reduced lease expense. ~$50m of lease expense savings is huge for a company that was doing $20m of EBITDA in F19.

The monthly operating results are in-line with Tuesday’s expected annual lease expense of $73m in F22 vs $118m in F19 - below are the projections for F22 from TUES cleansing materials (LINK to helpful slide deck from Cleansing Material 11/13/20):

And the remaining 490 stores have been comping well on higher average sales per store. Comps from remaining 490 stores the December 2020 quarter:

Less competition post-COVID:

Many retailers filed bankruptcy due to COVID-19 and many others are closing stores due to secular shifts. This list is long but a few relevant to TUES are:

Pier 1: Filed bankruptcy in February 2020 and is closing all 500 stores LINK

JC Penney: May 2020 filed bankruptcy, will close 250 of 850 stores LINK

Stage Stores: May 2020 filed bankruptcy, will close 738 stores LINK

Stein Mart: August 2020 filed bankruptcy, will close all 280 stores LINK

Trends in off-price and home decor are strong

TUES categories are performing relatively well:

Off-price and treasure hunt is doing well

Off-mall doing relatively well

Home goods doing well and over 50% of TUES sales are home related. $TUES F20 revenue breaks out to:

Textiles 21.6%

Housewares/Food 18.5%

Home Decor/Furniture 18.0%

Crafts/Toys/Pets 13.8%

Seasonal 12.1%

Other 15.9%

Recent Reports from Peers:

$TJX - TJ Maxx 11/18/20:

HomeGoods open-only comp up 15% in the Oct20 quarter

$HOME - At Home 12/1/20:

3Q Oct20 comp growth was up 44%

“While our strength was broad-based and all departments comp solidly positive: wall decor, textiles, accent decor, kitchen and entertaining and home organization were exceptional.”

“Based on quarter-to-date trends, we expect total Q4 comps to be in the mid- to high teens and are on track to deliver some of the best fourth quarter results in At Home's history.”

$BIG - Big Lots 12/4/20

Comps up 17.8% in the October quarter

Furniture sales increased 25% versus last year, with all departments driving double-digit comp growth. Upholstery and home office were both up 30%, with ready to assemble, mattresses and case goods, all up around 20% to last year.

QTD comps up low-double digits as of 12/4/20

$MIK - Michael’s Stores 12/3/20:

Comparable Store Sales increase of 16.3% for the October quarter

$KSS - Kohl’s 11/17/20: “Our home business remained strong during the third quarter with sales up 10% overall and up over 50% digitally. Our customers continue to show interest in the kitchen with solid demand for cookware, food preparations and kitchen electrics as well as our living spaces where sales increased in floor care and bedding.”

$OLLI - Ollie’s Bargain Market 12/3/20:

Comps up 15.3% in Oct20 quarter

QTD to 12/3/20, comps up low-single-digits

There's still a lot of deal flow out there. Bankruptcies have happened. There's a lot of excess inventory that has been canceled by other retailers. So the closeout environment is as robust as it's ever been.

TUES Inventory Opportunity

Inventory levels in September were down ~60% year-over-year which led to sales trends slowing. As inventory levels increase, sales should follow.

“We believe the decline in comparable store sales was due in part to a decrease in store level inventory. Average inventory per store was down approximately 57% for the first quarter of fiscal 2021 (Sept 2020 quarter), compared to the same period last year.” (Source: 10Q filed 11/6/20)

“This decline was partially due to the strength of sales immediately post re-opening as well as our inability to restock stores rapidly. Store level inventory challenges were due in part to the closure of much of our merchant and supply chain operations during the height of the spring COVID outbreak as well as pandemic-related disruptions to the supply chain. (Source: 10Q filed 11/6/20)

Exiting BK will give vendors more confidence to sell to TUES. As disclosed in the monthly operating results, inventory purchases have increased significantly in the past three months:

What is it worth?

Valuation of Peers - EV/EBITDA multiple ranges on next-12-months estimates over past three years:

TJ Maxx (including HomeGoods) $TJX: 10-17x

Ross Stores $ROST: 11.5-18x

Burlington $BURL: 12-21x

Ollie’s Bargain Market $OLLI: 16.5-29x

Big Lots $BIG: 5-8x

Potential Valuation Ranges for $TUES:

TUES projections were filed in the Amended Disclosure Statement Filed 11/4/20 (Source: Docket #1495 beginning on page 188) as well as in the Cleansing Materials filed 11/13/20 with SEC below (SOURCE):

Assumptions:

Total shares of 95.1m: Includes current shares outstanding of 46.9m plus 38.2m coming from the rights offering plus 10m warrants at $1.65 (Source)

Net cash of $40.5m. The normalized balance sheet at 12/31/21 is expected to be $42m cash and $28m debt plus an additional $10m of incremental proceeds from the real estate sale on 12/7/20 (noted above) as well as $16.5m from 10m warrants at $1.65.

No value ascribed to the $140m NOL

Note: actual EBITDA in F19 was $20m and management had guided for “EBITDA to improve meaningfully” in F20

Cash Flow

TUES is projecting $35m of operating cash flow and $7.6m capex in F21 and $53m operating cash flow and $5m capex in F22. If TUES does $48m of FCFE in F22, the free cash flow yield is 38% (with stock at $1.50 and 85m shares out)

Are these estimates realistic?

$TUES did $20m of EBITDA in F19 and was expecting EBITDA to grow in F20 prior to COVID. $TUES has already cut ~$50m of rent expense and closed 199 stores that were likely loss-making. So adding the $50m rent savings to $20m run-rate EBITDA gets to $70m of EBITDA prior to other cost cuts, so modelling ~$50m EBITDA does not seem crazy. And $TUES’ target of 6.7% EBITDA margin is well below $TJX at 12.7% in 2019, $ROST at 15.6%, $BURL at 11.1% or $OLLI at 13.3%. Plus management might have an incentive to set a low-bar they can exceed in order to maximize their incentive plan.

Below is TUES bridge to $52m EBITDA in F22 as disclosed in their cleansing materials from 11/13/20:

Downside protection

Valuation is low on realistic assumptions (cost cuts are already implemented)

Insiders own meaningful amounts of stock and have an incentive plan with equity upside

40 buyers expressed in interested in TUES during BK process - from Docket 892 on 9/18/20:

The Debtors further disclosed that they have entered into non-disclosure agreements with forty prospective buyers who have been granted access to a data room, provided substantial follow-up information to facilitate due diligence requests, and held management presentations with certain of the potential acquirers and that the Debtors have received indications of interest and non-binding letters of intent from a number of parties.

$140m NOL relative to the ~$130m market cap which could have value to an acquirer

Osmium is injecting fresh capital invested in business and likely other investors are interested in providing capital if needed

Balance sheet now solid and should be net cash in the coming quarters

$110m asset-backed lending credit facility

Better results coming with more inventory in the stores, better merchant, and easy comparisons

Catalysts

December 22, 2020 the Judge confirmed exit from bankruptcy (Source: Docket 1909 and Press Release: LINK)

Current buyers of shares MIGHT have the opportunity to participate in rights offering at $1.10 (please verify to your own satisfaction). Recent 8K has additional info including “The Company currently anticipates the “rights offering/exchange determination date” will be the close of business on January 4, 2021”: LINK

$TUES could re-list on the Nasdaq, opening to more potential buyers of the stock

Once on the Nasdaq, it is possible $TUES would be included in indexes, creating further demand for the stock

Easy compares coming as TUES had limited inventory through BK and economy re-opening

Vaccine/end of COVID is positive for TUES customer who is 53 years old on average and may have been cautious leaving house to shop in-store

Better inventory now that $TUES is emerging from BK and vendors are open to doing business again which could drive sales

New merchant as of December 2019 with great experience and an improved team can make a difference with better merchandising

Potential new CEO with operational background could be positive

Potential to expand online similar to $TJX announcing HomeGoods e-comm roll out in 2021 - from 11/18/20:

“To both leverage our strength in the home category and capitalize on our market share growth opportunities, we are pleased to share that we plan to rollout e-commerce on HomeGoods.com later next year. “

Additional fiscal and monetary stimulus in 2021 could help Tuesday Morning’s customer

Potential sell side coverage

Risks

Retail is extremely competitive and over-stored

Company and analyst projections could be wrong

Financing might not be available or at onerous terms

TUES filed for Chapter 11 Bankruptcy in May 2020

Osmium Partners will be a significant shareholder and have significant influence over the company

Every risk that comes with investing in small cap and retail stocks

If you have any incremental insights, please reach out: @RationalResear

For credibility purposes, recent write ups on JWN and TTSH are here:

$TTSH from 9/27/20 (stock at $2.61): https://rationalresearch.substack.com/p/tile-shop-holdings-ttsh

$JWN from 9/7/20 (stock at $16.28): https://rationalresearch.substack.com/p/nordstrom-jwn

DISCLAIMER: Nothing here is investment advice. This is for informational purposes only. Do your own research.

Useful Resources:

Slide deck from Cleansing Materials filed with SEC on 11/13/20: https://www.sec.gov/Archives/edgar/data/878726/000110465920125142/tm2035026d2_ex99-1.htm

Bankruptcy Dockets: https://dm.epiq11.com/case/tuesdaymorning/dockets

Amended Disclosure Statement: Docket 1495, Financial estimates begin on page 188

Key board members and management: Docket 1879

“PLAN CONFIRMED”: Docket 1909

Monthly Operating Reports - month of November 2020 is here: https://www.sec.gov/Archives/edgar/data/878726/000110465920138088/tm2038936d1_ex99-1.htm

Press release 12/23/20 confirming bankruptcy emergence by the end of December 2020: https://www.globenewswire.com/news-release/2020/12/23/2150195/0/en/Tuesday-Morning-Announces-Confirmation-of-Plan-of-Reorganization.html

Excellent report. Thank you for sharing it. I've visited several Houston stores the past week. I am amazed by the demographic. These are people who truly enjoy shopping. My guess is half the customers carry Costco cards too. With fresh inventory returning regularly, their customer base will likely return to regular numbers because treasure hunting provides a better dopamine hit than clicking on Amazon links does. The lack of full inventory during BK may result in one more sub-par quarterly report, but the store help I talked to said that business was back to normal and shipments are coming in again.

Any update on this one? Breathtaking decline from the peak, but I guess the rolling over of consumer spending really hurt.